Despite China’s selective restructuring and strengthening of its regulatory institutions/rules, China has not directed its efforts toward establishing liberalized capitalist markets.1) This is implicitly ensured by Premier Wen Jiabao, who claims that while adopting regulatory measures over the last two decades, China has gradually introduced “a system that suits China’s special features.”2) In other words, China’s goal of economic regulation is to create a powerful and efficient party-state run economy centered around strategic industries.

Nevertheless, the world (particularly international institutions) eyes and values China from Western standards. For example, some argue that regulatory reform in China definitely has not gone well because China failed to establish an arm’s length regulatory apparatus.3) Others give China credit for making impressive progress in competition policy, market opening, as well as establishment of sectoral regulatory authorities in infrastructure sectors, but conclude that much remains to be done.4) This does little to explain China’s system of economic regulation and appraise its performance, for China’s leadership has skillfully used the Western-centered rules and experiences without adopting them.5)

Beijing has keenly strengthen comprehensive party-state institutions in supervising the functions of a range of sectoral regulatory authorities—which started to emerge in 1992 with the creation of the Securities Regulatory Commission—and in controlling the structure of the market.6) Moreover, its primary emphasis is on fostering China’s biggest state-controlled corporations (nicknamed “national champions”) and orderly competition rather than embedding accountability, transparency, and full-scale market competition. Such distinctive features challenge the relevance of the conventional framework in reviewing the performance of China’s regulatory reform.

One should not assess China’s regulatory reform via the standard of an idealized independent regulator model, but rather analyze what the Chinese leadership has actually attempted and accomplished through the reform. Armed with its regulatory mechanism, goals, and tools in forming economic regulation systems, China has been quite successful in empowering supraregulatory bodies that supervise sectoral regulatory authorities, as well as in transforming state-owned large industrial groups into “global” champions beyond the national markets. The consistent policy of “orderly” competition as a new type of industrial policy has played a key role in doing so.

1)For the dynamic characteristics of the Chinese regulatory reform in the age of the World Trade Organization (WTO), refer to Margaret Pearson, “Governing Business of Governing Business in China,” World Politics 57-2 (2005), pp. 296-322; Margaret Pearson, “Variety Within and Without: The Political Economy of Chinese Regulation,” in Scott Kennedy (ed.), Beyond the Middle Kingdom: Comparative Perspectives on China’s Capitalist Transformation (Stanford: Stanford University Press, 2011); Yukyung Yeo, “Between Owner and Regulator: Governing the Business of China’s Telecommunications Service Industry,” China Quarterly 200 (December 2009a); Yukyung Yeo and Martin Painter, “Diffusion, Transmutation, and Regulatory Regime in Socialist Market Economies: Telecoms Reform in China and Vietnam,” Pacific Review 24-4 (September 2011). 2)Fareed Zakaria, “Meeting with World Leaders at the United Nations,” CNN (28 September 2008), available at

Ⅱ. Modern System of Economic Regulation

According to the Organization for Economic Cooperation and Development (OECD),7) “one of the most widespread institutions of modern regulatory governance is the so-called independent regulator,” although independent regulatory agencies are far from the only institutional option for the regulation of markets.8) To some extent, contextual factors such as politicaleconomic tradition or leadership choice bring about variance in practice, yet much of the literature on regulation of market economies (particularly in infrastructure sectors) has assumed ideally that institutional organizations that regulate markets should be independent of government and firms in order to prevent “unfair competition.” This globally idealized model of economic regulation has been diffused and adopted.9) Institutionally, the model emphasizes the creation of an independent regulatory agency that monitors and enforces the compliance of rules in governing markets; in so doing, these agencies are entrusted with the authority to promote and oversee fairly market-oriented competition, enforce licenses, and sometimes control prices.10) In normative terms, its main task is to see that market competition is fairly regulated (“regulation-of-competition”). Moreover, such a model has been recommended and introduced by international institutions such as the World Bank, World Trade Organization (WTO), and OECD that strongly advocate for neoliberal economic policies.

However, there is a “conceptual issue” that challenges the extension of the validity of the independent regulator model, especially in transitional economies. The formal organizational position of regulatory agencies in China is often subject to the oversight of supra-regulatory authorities and their instructions, largely due to China’s communist past. China’s regulatory regime is a good example of this case. “Regulation” and “independent regulatory agency” are notable in that the way of conceptualizing these notions may embed the ensuing institutional and normative preferences. For a regulator to be an independent agency, is should at least 1) “have its own powers and responsibilities under public law; 2) organizationally get separated from ministries; 3) be neither directly elected nor managed by elected officials.”11) Yet, the continued political controls from the party-state in transitional economies may allow for other forms of institution (e.g., supraregulatory authorities in China) by relaxing these “minimum” requirements. What is more, in one regime, regulation may be “a set of authoritative rules that often accompany administrative agency to monitor and enforce compliance,” whereas it also refers to “the aggregate efforts by state agencies to steer the economy” in other political economies.12) Such variances in definitions are important because they imply a latent difference in shaping political-economic institutions of market regulation: the former indicates a more minimalist role of the state and privatization, while the latter invites a more interventionist state in the market and the possibility of public ownership. This begs the following questions: Is the globalized ideal reform model appropriate to assess China’s regulatory reform? If not, is there one that is?

7)OECD, Regulatory Policies in OECD Countries: From Interventionism to Regulatory Governance (Paris: OECD, 2002), p. 91. 8)Fabrizo Gilardi, “Institutional Change in Regulatory Policies: Regulation Thorough Independent Agencies and the Three New Institutionalism,” in J. Jordana and D. Levi-Faur (eds.), The Politics of Regulation: Institutions and Regulatory Reforms for the Age of Governance (Cheltenham and Northampton, UK: Edward Elgar, 2004). 9)Fabrizo Gilardi, “Spurious and Symbolic Diffusion of Independent Regulatory Agencies in Western Europe,” paper presented at the workshop The Internationalization of Regulatory Reforms, Center for the Study of Law and Society, University of California, Berkeley, 25-28 April 2003; David Levi-Faur, “The Global Diffusion of Regulatory Capitalism,” The Annals of the American Academy of Political and Social Science 598-1 (2005). 10)Mark Thatcher, “Delegation to Independent Regulatory Agencies: Pressures, Functions, and Contextual Mediation,” West European Politics 25-1 (2002), p. 126. 11)Ibid., p. 127. 12)Jacint Jordana and David Levi-Faur, “The Politics of Regulation in the Age of Governance,” in J. Jordana and D. Levi-Faur (eds.), The Politics of Regulation: Institutions and Regulatory Reforms for the Age of Governance (Cheltenham and Northampton, UK: Edward Elgar, 2004), p. 3.

It is often said that “the emergence of the regulatory state is much more than a by-product of neo-liberalism.”13) In China, the rise of the regulatory state since the 1990s has been driven by the party-state’s careful efforts to introduce market-oriented institutions and norms (by replacing the planned economy systems), while simultaneously strengthening the party-state’s authority for economic governance. Accordingly, it would be incorrect to value China’s regulatory reform only by relying on the globally idealized independent regulator model. Equally important is that the Chinese leadership has far from tried to follow such a path. China’s reform efforts have been quite successful in shaping its own system of economic regulation. Although sectoral regulatory authorities have been established, the goals of the leadership are to strengthen the institutional capacity of hierarchically structured supra-regulatory bodies, and normatively to create national champions and control the governance of competition in strategic lifeline industries. The outcome of these imperatives is discussed below.

1. Empowered Supra-regulators: NDRC, SASAC, and CCP

Institutional capacity is “the ability to formulate and carry out policies and enact laws.”14) Relying on this definition, this study argues that the capacity of supra-regulatory bodies in China’s lifeline industries has been empowered through the reforms of economic regulation.15) Supra-regulators in China refer to institutional organizations that supervise a range of sectoral regulatory authorities. They include the National Development and Reform Commission (NDRC), the State-owned Asset Supervision and Administration Commission (SASAC), and the Communist Party. Although neither the arm’s length regulatory apparatus nor market-chosen competition has been substantially institutionalized, Beijing has made it to what the leadership has planned to create: a state-led regulatory regime.

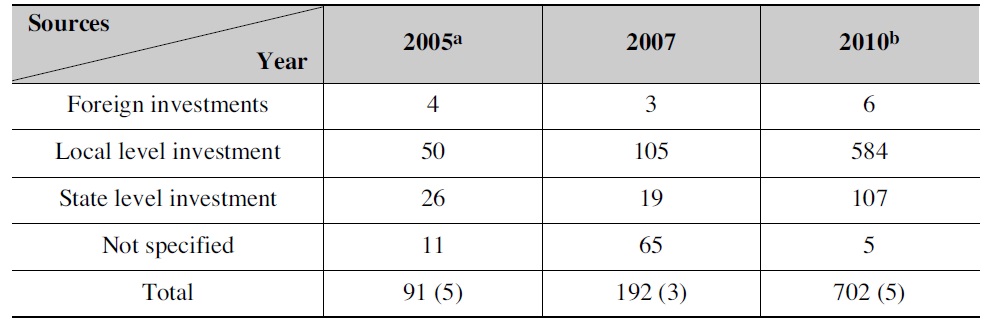

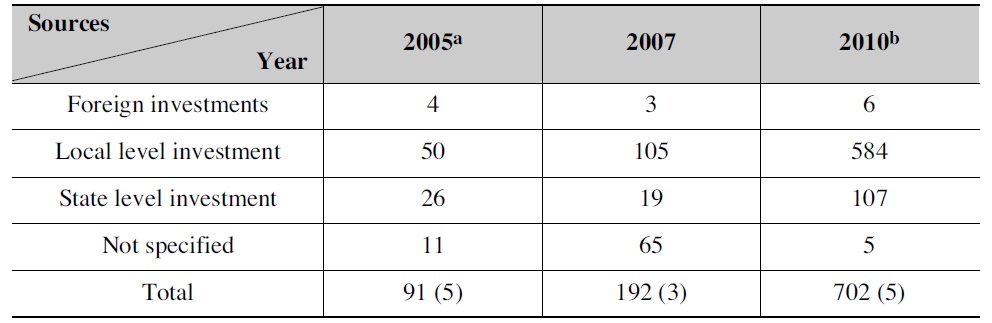

The National Development and Reform Commission evolved from the former planning agency over the last two decades. The NDRC has been transformed into a supra-regulatory agency responsible for guiding the macro-level development directions, not directly control as the planning agency did. NDRC formulates policies for economic and social development, and offers “indicative” planning by laying out direction and objectives, such as five-year plans.16) Although the NDRC-led five year plan no longer sets a specific target quantity of production or for the distribution of resources, it still sets developmental goals. Taking responsibility for maintaining macroeconomic stability, NDRC’s authority to endorse large-scale investment projects, oversee prices in infrastructure sectors, and create industrial policy all constitute its key levers of regulating market forces. For example, the pricing department of the NDRC sets price ceilings for goods and services and making rules against price manipulation. The right to approve investment also enables the NDRC to adjust the industrial structure by endorsing more energy conservation projects while reining in overcapacity sectors in which repeated constructions and blind investment are rampant.17) Moreover, as the 2008 global financial crisis brought the issues of rising inflation and unemployment to the center’s close attention, China rolled out the stimulus program with mounting infrastructure investment plans and industrial restructuring initiatives. This stimulus package indeed provides the NDRC with more opportunities to exercise regulatory control over both the scope and nature of investment by engaging in designing, developing, and approving projects from their inception. For example, the number of investment proposals endorsed by the NDRC increased from ninety-one in 2005 to 702 by 2010 (see Table 1).

[Table 1.] NDRC’s Approval of Investment Projects, 2005-2010

NDRC’s Approval of Investment Projects, 2005-2010

At the same time, though the primary investment in the stimulus program goes into the building of infrastructure, 12 percent of the total investment is assigned to long-term technological innovation and restructuring to stimulate applied industrial research and adjustment.18) Following up such proposals, the state-backed development plan of six new strategic industries, including energy, biotechnology, and information-technology, was also announced by Premier Wen Jiabao in the 2010 Report of Government Work.19)

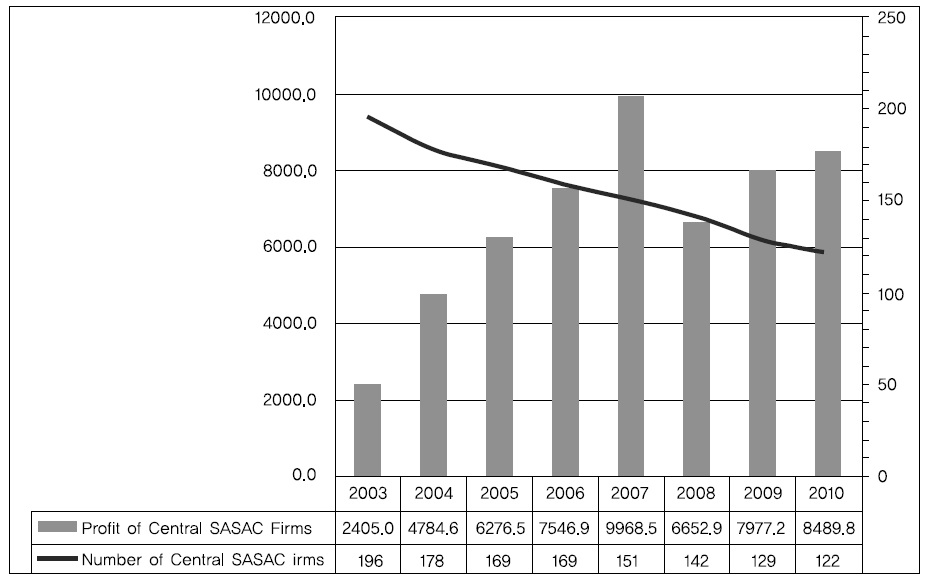

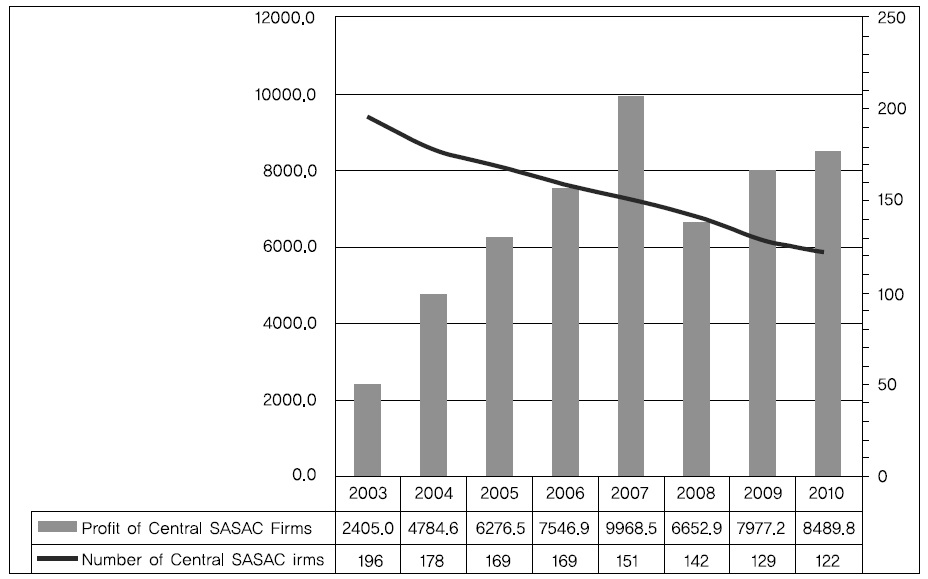

Another comprehensive regulator is the State-owned Asset Supervision and Administration Commission, whose main task is to oversee the central state firms’ financial performance, including redistributing and enhancing the assets’ value. Since the creation of the SASAC, the increased profits of central state firms (see Figure 1), the substantial progress in market consolidation, and the new rules for the dividend evidences how SASAC has enhanced its capacity for supervising the business of large state-owned enterprise groups. In China, as creating few but powerful large national companies has been a key principal of reform of large state-owned enterprises (SOE), market consolidation becomes crucial; under the leadership of SASAC, the number of central state-owned enterprise groups was reduced from 196 in 2003 to 122 in 2010. Given its early claim for consolidating them to around 100 by 2010, it would be fair to say the goal is nearly achieved. Moreover, such a consolidated market structure has contributed to turning large central SOEs into profit-making firms. According to SASAC, “between 2001 and 2006, Chinese SOEs have seen profits grow at a compound annual rate of 28 percent, with a few resource groups reaping the biggest gains.”20) In the wake of the 2008 financial crisis, the profits of central state firms have risen from RMB 2,405 hundred millions in 2003 to RMB 9,969 hundred millions in 2007 (see Figure 1). As state groups have become some of the biggest profit-makers, SASAC was able to propose a dividend policy for central SOEs in 2007, hoping that “the payment of SOE dividends into public coffers will provide a source of fiscal income and curb wasteful spending.” Likewise, the improved financial performance of central SOEs has placed SASAC in a better position to push forward the policy of dividend payments as a new regulatory measure.

The decision to impose dividends for central SOEs is a remarkable step in the central leadership’s efforts to rebalance both the overcapitalized state firms and distribution of wealth, which signals a more active role for the SASAC in managing the state assets When the SASAC emerged in 2003, its main concern was to protect its crucial assets by optimizing market structure with large state groups. The dividend policy of late that calls for the increased ratio from 2010 might be a good indicator of the changing weight of SASAC’s function from simply “securing/enhancing” state assets to “redistributing” them. In December 2010, the SASAC issued a revised scheme that requires the largest central state firms to pay larger dividends than before to “help rebalance the economy and funnel more money into the country’s underfunded public services.”21) Accordingly, the first-tier of state enterprise groups, which earned huge profits in recent years, is required to “pay 15 percent of their post-tax profits to the government, up from the current dividend of 10 percent.”22) These include the parent company Petro China, Sinopec, China Mobile, and China Telecom. This dividend scheme also discourages highly profitable state groups from reinvesting the profits in property or stock markets for speculative purposes.23) In short, a range of policies that SASAC has proposed and administered increased its regulatory capacity; the growth in the profits of central state firms not only demonstrates its successful supervision of state assets, but also provides SASAC with the financial grounds for imposing the dividend for them.

To some extent, SASAC’s dividend policy for large state groups has significant implications for the leadership’s changing goals of market regulation, from steering the economy to transforming its nature and system into a more balanced one. What is more, the dividend scheme has certainly created a space for SASAC to play a larger role both in curbing imprudent overinvestment of central state firms and strengthening social safety nets, so that the rebalanced economy may lead to sustainable growth.

A third and often little documented aspect that makes China’s regulatory regime distinct is the supervisory role of the Communist Party. The party’s

Although economic governance has been remarkably institutionalized in theory, leading small groups still remain crucial in the areas of compelling national interests, such as finance and security.25) By sitting on the top of supra-regulatory bodies (NDRC and SASAC) as well as sectoral regulatory authorities (e.g., Chinese Securities and Regulatory Commission and Ministry of Information Industry26)), these leading small groups are responsible for supervising “major strategies, policies, and countermeasures for the national responses to a range of issues, as well as laying out unified arrangements and coordinate the resolution of major problems in coping with raised issues.”27) For example, the central finance leading small group (

For its part, the Central Organization Department continues to control key posts in both government (regulatory agencies) and state firms, which is another heart of the party’s capacity to overhaul the business of regulators and state companies.29) Regardless of how much the system of appointment procedures has been institutionalized, it is

2. From National to Global Champions

It was not market liberalization but the norm of “grasping large, letting go small” that has been central in guiding the regulatory reform of strategic infrastructure industries including power, finance services, and telecommunications. In doing so, Beijing has made great efforts to foster large and successful state-owned enterprise groups that are able to lead each sector.33) This is in part because “the Communist Party has fretted over its dwindling influence as the state sectors” contribution to gross domestic product fell from nearly 100 percent in the early 1980s to around 30 percent in 2000.”34) As discussed earlier, the number of state firms under SASAC’s oversight fell from 196 in 2003 to 122 by the end of 2010. Moreover, as these state-owned national champions are increasingly appearing on

[Table 2.] Total Number of Chinese State Firms Ranked in Fortune Global 500, 1996-2010

Total Number of Chinese State Firms Ranked in Fortune Global 500, 1996-2010

There is some debate as to what this increase reveals: does it tell us about the competitive edge of Chinese state firms, or simply about Beijing’s power in the global market? For instance, skeptics assert that both impressive profits and sales revenue of China’s listed firms are not from the firms’ ability to offer innovative products, but rather from their state-backed monopolistic market position.37) Yet it should be noted that the large Chinese state firms that enjoy monopolistic position in markets are not necessarily uncompetitive in terms of their business sophistication and innovation. According to the Global Competitiveness Report 2010—2011, China ranks 26th in innovative business among 150 countries;38) its performance in business innovation is valued as more competitive than Hong Kong (29th) and India (39th),39) where private companies lead the markets. The contending views on global competitiveness of China’s big state firms are also salient, which stems from a disagreement over the concept of “global competitiveness.” Whereas Beijing, by putting emphasis on the “global,” tends to perceive a “globally competitive company” that owns “vast assets, cash-flow, and claims on resources and markets in other countries,”40) foreigners insist that a company’s real competitiveness lies in its own technological innovation, not in global outreach. The importance of a balanced approach is also called for because the firm’s competitiveness in China depends on the sector and the region beyond the privilege of market monopoly resulting from state ownership.41) Michael Enright argues that “China’s rise show us we must change traditional notions of competitiveness to include not just what a nation has, but also what it can attract.”42)

China’s great market potential, labor force, and access to Hong Kong clearly enable China to attract complementary resources on a noncompatible scale and to raise its global competitiveness. Regardless of such opposing views or changing notions of global competitiveness, it is indeed remarkable that an increasing number of Chinese state-run oligopolists are becoming global giants that are ready to outcompete on the international playing field.43)

3. Orderly Competition: A New Version of Industrial Policy?

China’s competition policy in economic regulation does not necessarily mean full-scale liberalization and openness to the market. Although there is greater tolerance for the range and space for the market than before, what China’s regulatory authorities have actually promoted in strategic lifeline industries is

In a way, China’s orderly competition policy now becomes a new version of industrial policy First, this state-chosen orderly competition may allow policymakers and regulators to make decisions on how competition is governed. Second, the main concern becomes not to correct market failure and oversee anticompetitive behavior, but to steer the economy by preventing excessive competition, which invites the more explicit and active role of states. Third, growing out of this orderly competition, China’s newly structured state-owned oligarchies have come to outcompete international firms. This is particularly relevant in strategic infrastructure industries where state regulation has formed the structured competition. In effect, Edward Steinfeld argues that China’s industrial policy is moving its foci to creating environments, not to nurturing firms.47) By creating environments, China’s orderly competition indirectly contributes to strengthening Chinese firms’ cutting edge. As Levi-Faur notes, this type of competition policy harbors the rise of neomercantilism in that state-led regulation does not endorse head-tohead competition and entirely free markets.48)

13)Ibid., p. 2. 14)Francis Fukuyama, State-building: Governance and World Order in the 21st Century (Ithaca, N.Y.: Cornell University Press, 2004), p. 8. 15)For more information, refer to Margaret Pearson, op. cit. (2007). 16)For its official functions, see the commission’s brief explanation at

Over the last two decades, China has embraced the globally advised model of regulatory reform but attempted to institutionalize a system of market economy centered on large state-owned enterprise groups under strong party-state supervision. In doing so, supra-regulators have made great efforts to create globally competitive large state firms under carefully orchestrated orderly competition. As this analysis makes clear, particularly in the wake of the recent global economic downturn, there is far more merit in revisiting the Chinese regulatory reform than to conclude that it has failed. Such a reexamination, with an eye to both successes and stumbles, allows a better appreciation of both the contributions and the flaws in China’s regulatory regime itself, as well as making us aware of how and in what ways it may present an alternative path to the ongoing forces of market liberalization.

In fact, at least three points remain worthy of underscoring, regardless of whether China’s own experiences retain a possibility of being exported. Most notably, the system of Chinese economic regulation in strategic lifeline industries draws attention to the ways in which the market economy could be successfully pursued under the continued or even enhanced party-state supervision. Even after the global financial crisis of 2008, the comparative macroeconomic stability of China under close state oversight of financial institutions proves to be largely superior to liberal capitalist markets. Second, China’s regulatory system clearly demonstrated that regulatory reform could advance along more than one path. The so-called ideal model fails to take into account how the domestic conditions, such as the lingering communist past, may generate its own regulatory regime. Indeed, the Chinese experience, to some extent, “reinforced the more general argument that there was more than one way to organize a capitalist economy. This serves as a reminder that there is also more than one path to market liberalization.”49) Lastly, China’s globally rising state enterprises have drawn new attention to the significance of the inherent political power in global competition, as the level playing field on which companies compete becomes more denationalized. In addition, this also opens up a possibility of redefining the conventionally accepted concept and ideas. For example, over the past quarter century, industrial policy had been considered a bad idea because the allocation of resources in markets is too complicated for the government to implement centralized economic policies and strategies. Yet, industrial policy is back, and its virtues showcased.

As discussed, the central leadership in China claims that China’s successful transition to a market economy demands not only the invisible hand, as the ideal type of independent regulator model prioritizes, but also a visible one in order to maintain macroeconomic stability (such as inflation and unemployment rate). Hence, the conventional approach to the subject appears to be ill-positioned to make a reliable evaluation of what China’s regulatory reform has accomplished.

49)T. J. Pempel, “Revisiting the Japanese Economic Model,” in Saadia Pekkanen and Kellee Tsai, Japan and China in the World Political Economy (New York: Routledge, 2005), p. 43.