Almost as a contradiction in terms, in India, the claims and efforts towards achieving inclusive growth as the policy objective have been upset by facts on ground which confirm a growing syndrome of exclusion in terms of both options in and rights to livelihood, particularly in rural areas and small towns. Any discussion on the rural economy and livelihood options must engage with the question of resource endowments, land being the prime most entitlement followed by various infrastructure (Das, 2002). The findings of the just published Socio-Economic and Caste Census (SECC) 2011

The non-farm manufacturing enterprises in rural India are almost entirely (about 95 per cent of units) in the unregistered or informal sector. This status per se acts as an important barrier to access any state-sponsored business services including energy, physical infrastructure and finance that would facilitate innovation activities in these enterprises. With the exposure of local economies to higher stages of markets, multiple forms of technology and varieties of institutional cobwebs, there has been a crisis-like situation staring at the survival and prospects of traditional craft-based activities, which are typically found in areas that provide for human skill/knowledge, physical / natural resources and a certain semblance of an assured local market, if not beyond. All these - markets, institutions and informality - have pushed innovation to the margins as entrepreneurship has been reduced to eking out a living, more as a subsistence option rather than a business activity. This is despite the intervention by the state in several ways through announcing schemes and programmes addressing enhancing product and process standards of the artisan enterprises.

A close look at the emergence and perusal of state policies on industralisation at the national level makes it clear that rural industrialization never figured as a significantly potential sector that required wholesome attention. It is interesting to note that even as in the Industrial Policy Resolution of 1956, cottage and small scale industries were recognized to generate huge employment potential, and facilitate narrowing of regional income gaps and utilize available capital and skill. The sector was assigned a secondary role of supporting the large enterprises as their appendages. Despite the evocation then that India’s industry would be “walking on two legs”

Given the historical and systematic neglect of rural industrialization from a policy perspective, this paper attempts to explore the nature of institutional constraints to innovation. This has been undertaken through primary survey based case studies of five rural artisan clusters in as many Indian states. The unit of analysis of this study has been the rural cluster which is faced with a common set of challenges and opportunities in business. In fact and moreover, the cluster embodies the dual entity of a sector and the space representing dynamics of the enterprise collectivity not just from the subsector point of view but also the strengths and infirmities of the space of working of the firms. This would include aspects of entrepreneurship, local infrastructure, governance structure and informal institutions active therein. By focusing on the cluster one is in a better position to comprehend and assess institutional constraints to innovation. A particular concern in this enquiry has been to assess if the innovation systems have been inclusive or pro-poor, in terms of access to available options in innovation be that technological or institutional; this focus per se is useful in understanding the innovation ecosystem around the artisan clusters in rural locations. The five clusters concern handicrafts, handlooms and artisan skill based activities in the states of Karnataka (leather footwear), Odisha (appliqué), Madhya Pradesh (handloom), Rajasthan (clay-terracotta), and Assam (bamboo craft).

The subsequent three sections of the paper offer a critique of the extant policy approaches for rural industrialization by underscoring inadequate understanding of the dynamics or specificities of the rural industrial sector, inattention to skill and capacity building and the constricted cluster development programmes. Findings from the field surveys of the five clusters are presented in the subsequent section dealing with cluster characteristics and constraints to innovation. The role of institutions, both state and non-state has been discussed in ensuring broad-basing innovation in the rural artisan clusters. Concluding observations summarize the discussions and suggest possible and relevant changes in intervention aimed at rendering innovation inclusive for the rural enterprises.

II. Policy on Rural Industrialisation: Inadequate and Insipid

The continuance of assigning a subsidiary or subordinate status to rural enterprises in the policy process was carried through several national industrial policy statements, 1970s onwards. For instance, the Industrial Policy Statement of 1977 aimed to encourage spread of rural industries across space so that it would engage largely in meeting the local demand for a variety of goods and services. Although this approach visualized developing close linkages with the farm sector and rural resources the absence of a clearly spelt out strategy as to how the existing institutions would be operationalizing policy instruments remained a non-starter. Moreover, the Industrial Policy Statement of 1980 rambled its priorities of promoting “backward” regions through setting up nucleus plants that had nothing to do with rural enterprises which continued to suffer negligence (Inoue, 1992, 95). Similar apathy against rural industries, particularly, the artisan sector was palpable in the so called New Economic Policy that was announced in the early 1990s when economic reforms and liberalization were adopted as the macroeconomic framework for national growth. With increasing emphasis upon external orientation a large number of products in the artisan sector hardly received any attention in improving the quality and processes. The absence of recognition that the artisan sector being deeply embedded in the informal sector required special attention whether in terms of easy access to bank credit, technology upgradation, linking with newer markets and skill enhancement was a major shortcoming of the neoliberal growth strategy that India continues to pursue.

While policy support for rural enterprises remained both inadequate in coverage and insipid in responsiveness to some of the persistent constraints such as low levels of technology, skill, capital and markets, one expected the Micro, Small and Medium Enterprise Development (MSMED) Act promulgated in October 2006 to address their concerns. The so-called landmark Act, while promising to transform Indian MSMEs capable of being competitive in the global arena, had little to offer to rural enterprises. Similarly, another contemporary institution, namely, the National Manufacturing Competitiveness Council (NMCC) set up in 2004 had no reference to the rural enterprises even as the agency aimed at intervening in technology upgradation, design and intellectual property rights protection, marketing and skill upgradation. The NMCC focused on select modern subsectors that could participate in global production networks. That rural enterprises or clusters hardly mattered for the externally-oriented state policy could be gauged from the fact that the share of village industries in gross bank credit shows a declining trend during 1995-2013 and at least since 2001 the share has plummeted sharply. Despite the provision to allow for availing loans by the micro and small enterprises without any collateral, capital shortage has emerged as the most acute problem (leaving behind marketing or raw material procurement) faced by the rural unorganised enterprises (Nair, 2011: 130).

III. Education, Skill and Competence Building in Rural Enterprises

During the recent decades, amongst efforts made to build up skills and competence by artisans and workers the Scheme of Fund for Regeneration of Traditional Industries (SFURTI) administered by the Khadi and Village Industries Commission of the Government of India launched in 2005. With the creation of specialized Common Facility Centres (CFCs) in clusters in rural areas SFURTI was to aim for training with improved machinery, tools and processes. However, these facilities have remained mostly unutilized partly due to the fact that the manner of making products in given clusters following traditional skills, equipments and designs have not been understood adequately to be modified, if necessary. The distancing of the craftsperson from these external interventions has been recognized as an important deterrent to learning and capacity building by the workers in rural industries.

The National Commission for Enterprises in the Unorganised Sector (NCEUS) had recognized the significance of promoting various skills at the artisanal clusters and had proposed to impart these through the District Skill Development Councils (DSDCs). Unlike several government programmes in skill development, the NCEUS had expressed concern over the effectiveness of such interventions by pointing out that the level of education of the participant would be as important a factor as the quality of vocational training imparted. As it observed “purely artisan clusters will require co-ordination among artisans and recognition or education about the benefits of training, but costs will have to be borne by the state agencies under one of the programmes. Expenses and infrastructure for training of trainers can come under cluster based artisan improvement programmes that are located in clusters, again jointly under the cluster development programme and the DSDC” (NCEUS, 2009, 79).

An issue least focused in discussions on rural industrialization and especially on skill and competence building has been the very poor efforts, if at all, at collecting relevant and periodic information on all related variables influencing performance, survival and growth of rural enterprises. “Quite often the skills of artisans and those engaged in technical trade, as plumbers, fitters and electricians are inadequate and require upgradation. Modern hand tools, like micro cutters, drill machines and electronic screw drivers are not yet properly developed and when developed, are generally not used by artisans, craftspersons and other technical people. There exists great scope of developing appropriate hand tools, and training people in utilizing these tools. This would improve the product design and quality and, eventually, reduce time to finish a job. In other words, labour productivity would rise” (Biswas, 2011, 164-165). Despite numerous schemes and initiatives of the state and other private players to increase skill formation and building learning abilities, formidable constraints need to be addressed such as deficient social infrastructure, particularly, education, for the rural population.

IV. Rural Clusters and the Constricted Programmatic Initiatives

No discussion on Indian MSMEs, rural or urban, is now complete without reference to various cluster development programmes (CDPs) being implemented by several government and non-government agencies. Lauded in the policy circles and beyond as the strategy to upgrade MSMEs the functional mechanism and conceptual framework are deeply influenced by the cluster initiatives launched in India by the UNIDO way back in 1997. That these approaches are problematic, limited, biased and often not relevant to Indian realities have been pointed out time and again (Das, 2005a, 2005b, 2008 and 2011a and Das and Joseph, 2014). A particular issue of concern is that these approaches and schemes are largely sectoral in operational terms and, hence, fail to address quite a few structural and spatial limitations that have serious bearing upon learning, competence building and ensuring product and process standards, including those pertaining to labour. Further, the most important lapse of many such CDPs could be traced to an absence of understanding about varieties of informalities that act upon the performance of clusters. For the practitioners of these lines of cluster development initiatives, it is essential to appreciate local and regional infirmities within which clusters in rural areas and small towns function.

Most CDPs in India and related initiatives have been oriented towards participating in the global markets which requires concerted strategies in building firm competitiveness. While much less has actually been achieved in this direction due to a failure to address the implications of deepening of informaliiesy in enterprise functioning, the rural clusters are particularly at a disadvantage due to the nature of and demand for their products. The neglect of domestic markets (whether local, regional or national) in the policy thinking on cluster development has not augured well for a vast number of rural clusters which are often based upon localized skills and raw materials and could best serve domestic markets. Whether and how market platforms - which is an instance of a new institution, in fact - could be developed to address the concerns of rural clusters not only in accessing or processing raw materials but finding potential buyers with the support of the state and other relevant stakeholders, are yet to be brought up as policy issues.

Similarly, examples from the Asian economies exist that highlight innovative and locally-relevant strategies to build up the potential of rural clusters towards accessing larger markets through improved product and process standards. The Japanese approach of ‘One Village One Product’ (OVOP) or, its Thai recast ‘One Tambon One Product’ (OTOP) approach in rural Thailand is an excellent experiment in institutional innovation. These initiatives, also adapted in other Asian nations including, Philippines, China and Malaysia, have developed business strategies wherein self-reliance and creativity of the artisan form the basis of linking the local enterprises to wider (from local to global) markets. The conduits chosen to support the required networking with stakeholders and to access critical inputs and services as loan capital, product promotion, market assessment, etc. include conventional state agencies as relevant industry departments and banks but also unconventional agencies, for instance, educational institutions, national embassies abroad, high-end hotels and even international airlines. These several apparently unconnected (to the cluster business) agencies perform such crucial roles as data collection and analysis, advertising, marketing support, and exhibit products for foreign nationals so that product diversification could be introduced. Additionally, these initiatives include rewarding the artisan-champions at periodic intervals; this generates healthy competition, keenness to improve quality and, in fact, innovate at the enterprise level. These are significant out-of-the-box institutional and organizational innovations which would have much relevance to the Indian craft sector. “An important aspect of these efforts has been the increased emphasis on quality improvement on a constant basis. These programmes have amply established that clusters in villages and small towns must be competitive through adopting such management practices as kaizen (incremental but continuous efforts to improve quality) and that the key to business success lies in networking for product promotion and marketing” (Das, 2008, 25).

In so far as creating or enhancing the technological capability of a rural cluster is concerned the endowments of the spatiality would play a crucial role; considering bottlenecks in social, physical and economic infrastructure, enabling other institutions becomes an important component in any rural cluster promotion policy. For instance, poor or no innovation taking place in rural clusters could be attributed to the distinct disconnect existing between state-generated or sponsored technology and the need and conditions on ground to actually putting these into use. Given that there is hardly any interaction between the scientist and the artisan in a cluster, to take only an illustration to drive home the point, in the absence of institutions that would facilitate such a dialogue, it would be impossible to transfer the technology improvement in products and processes relevant to the craft to take place (Solanki, 2008). The rural technology institutes (RTIs) or the central government laboratories or university departments are yet to bridge this significant hiatus in what artifacts are designed/developed/invented and whether rural enterprises have a role in that process or whether they have developed for the enterprises.

Hence, creating a dependence syndrome by the rural clusters on what has been described as the ‘borrowed S&T’ precludes an opportunity to assess the strengths and weaknesses of existing innovation ethos, practices and, importantly, disincentives to innovate due to institutional dysfunctionality. While it is important to map, to begin with, options in learning, training, facilitating knowledge transfers and provisioning of business services one needs to appreciate the enabling or disabling environment for artisans to produce and conduct business as ‘equal’ citizens not as the receiver of ‘patronage’ by the state or dominant capital. The question that becomes central to policy making, in fact, concerns if existing institutions, rules and governance structures are adequate and empowered enough to ensure elimination of exclusionary practices and premises as working against the interests of rural enterprises. One such vital mechanism of shunning exclusion, clearly, is what we may term as ‘empowering’ firms in clusters in rural areas ensuring supply of electricity at the enterprise level (Das, 2007). This one-off intervention per se has the potential to transform the productivity and innovative capability of rural clusters significantly. An uncritical emulation of global cluster development ‘models’ without contextualizing and understanding the dynamics of clusters in rural areas or village towns - which account for a whopping over 94 per cent of all clusters in India

V. Cases of Clusters: Challenges and Implications for Innovation

While it has been common knowledge that clusters galore in rural India their functioning and performance show clear signs of the so-called ‘low-road’ syndrome with working conditions, product quality, access to business services/infrastructure and market spread often remaining sub-standard or grossly inadequate. Detailed surveys of five clusters across space and products in rural India constitute the core of empirical analysis for this study. While the selection of these five clusters was dictated by the time and resources available to undertake field research, attention was paid to render the choice as representative of the craft cluster world as possible. There was the consideration of space, hence, states chosen were from the south (Karnataka), east (Odisha), northeast (Assam), north/west (Rajasthan) and central (Madhya Pradesh) regions. Care was taken to include such subsectors that would represent handicrafts based upon distinct natural resources as raw materials (clay, bamboo and leather) and textile-based activities (handlooms and applique). It may be mentioned that the craft industry base of India is such that almost half these clusters (about 3000 in number) are handloom/ textile based and the remaining are handicraft products based on such diverse natural materials as wood, horns, leather, stone, metals (glass included), clay and variety of forest produce (reeds, canes, nuts, fruits, roots, gums, animal body parts, etc. included).

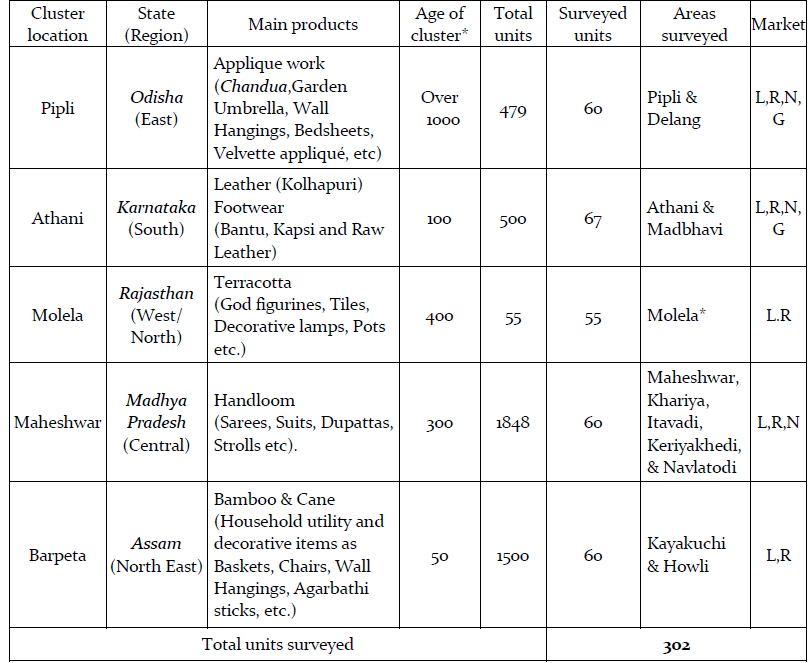

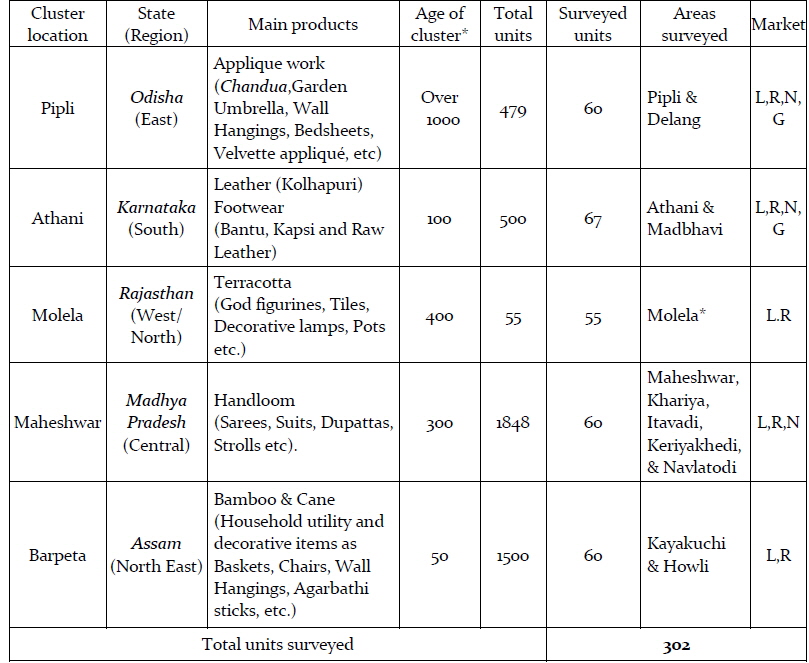

In Table 1, an idea regarding the selected clusters in terms of their age, products, markets have been presented along with the number of sample units interviewed using structured questionnaires. The idea was to choose about 60 units per cluster (setting a benchmark of existence of at least 50 units making up for a cluster) and a total of 302 units (almost all of these being microenterprises often operating from the homestead or shabby temporary structures). While Maheshwar and Athani may be termed as rural-towns, Pipli, Molela and Barpeta clusters were basically in the villages in and around the main locations. It may be interesting to note that products of Pipli and Athani do find a place in foreign markets. Although the former is through what may be termed ‘direct selling’ to (or, on the references of) the tourists, the latter has the support of a parastatal agency arranging to export a part of the output to buyers abroad. Nevertheless, in most cases of these select clusters, local and regional (state level) markets define their business.

[Table 1] Clusters studied in rural India

Clusters studied in rural India

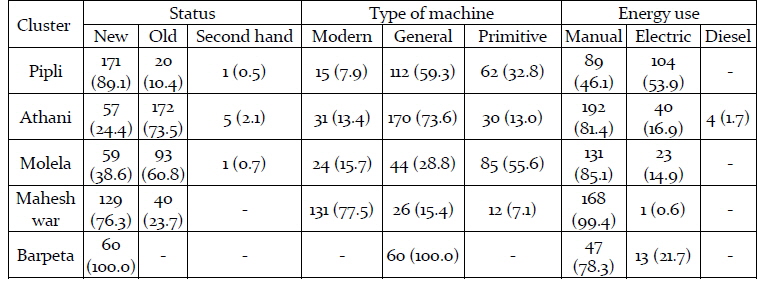

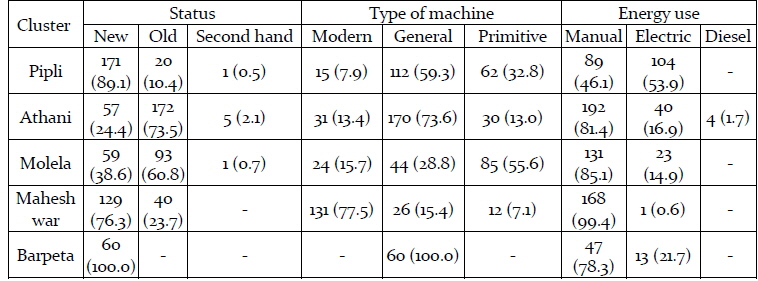

As in all these clusters the basic raw materials (textiles, leather, clay, bamboo, etc) are natural produce and mostly found locally, the processing of these has practically been by using traditional or primitive techniques and implements/tools. With an exception of a small proportion of footwear from the Athani cluster meant for exports, which have been made/processed using high-tech machineries as made available to the members at the private agency organised common facility centre (CFC), there have hardly been any significant change in the machinery/technology adopted for processing or manufacturing in these clusters. There, however, has been a shift to certain electricity-driven motors/machines as in case of Pipli or Maheshwar where the sewing machines and parts of looms have been run on electric motors. However, as Table 2 suggests, while most machines used are of general and primitive varieties, human power, craft and skill have been the source of much of the processing and manufacturing that take place in these traditional subsectors.

[Table 2] Type of machinery and level of technology at the cluster enterprises

Type of machinery and level of technology at the cluster enterprises

It needs to be stressed that unlike modern manufacturing the craft based products are deeply influenced by at least two critical dimensions, namely, raw material used and the specific techniques applied. The type of raw material could be a decisive factor in terms of whether one targets the local, regional/ subnational, national or global markets. The value to weight ratio and/or value to brittleness/perishability

Classified in a rather generalized manner the connotations of ‘old’ and ‘new’ machines have implications for the productivity of the enterprises and also, in certain cases, the processes and designs as well. These, however, vary across clusters and specific operations. While the applique cluster has benefitted to a large extent by switching over to modern sewing, embroidery and interlocking machines run by electricity, the bamboo craft and terracotta clusters are awkwardly stuck with very minimal and elementary tools that disallow the artisans to enhance productivity or improve processes.

It is in here that one needs to appreciate the distinctiveness of the artisan products and suggest suitable product and institutional innovations that would help enhance quality, productivity and, importantly, market reach. For instance, design support could be a significant manner of promoting the products, but building up facilities and relevant infrastructure towards, say, packaging, storage and transportation also matters. The case of the footwear cluster in Athani, to the extent the partner agency ToeHold from the private sector teamed up with the Government of Karnataka sponsored Karnataka Leather Industries Development Corporation Ltd (LIDKAR) to serve new export markets (Chatrapathy, 2005), is an instance of initiating innovations in products, design, processes, training entrepreneurs and marketing. Eventually, the nature of the market targeted feeds into the impulses for innovation.

While a particularly important issue in this connection is the lack of access to electricity by enterprises (as a reflection of the poor state of rural electrification efforts in India for all these decades since the Independence), it has been argued that most craft-based products from such rural clusters might lose market once the process is mechanized and/or conducted by using electricity replacing manual engagement by the craftsperson. In certain cases, as in Molela, the basic raw material (locally available clay) is facing a threat of dwindling supply as such land is no longer in the domain of free public access by the artisans. Similarly, the leather based clusters in Athani and Madabhavi have expressed concern over easy availability of the raw material with declining forest and open grazing land and even restrictions on acquiring, storing and processing raw hides and skin on grounds of environmental pollution. All these have implications for product and process innovation even at the cluster level and factor incomes, ultimately.

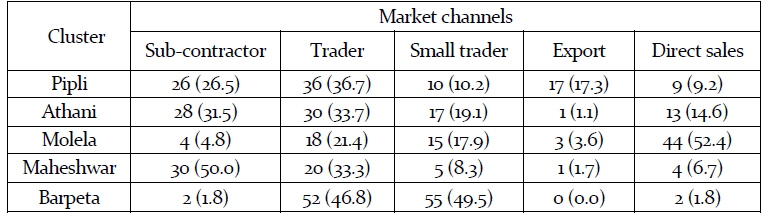

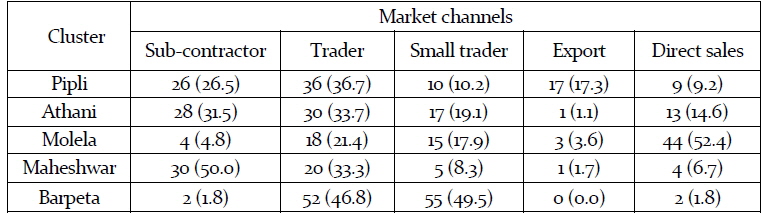

Unless special efforts, including by the state, come in a big way promoting their products in the hitherto inconceivable markets that would offer greater margins to the producers in the rural enterprises, there would be little incentive to innovate. As obvious from Table 3, the market channel that remains commonly available to the small producers of these clusters are both big and small traders. Even the domestic market remains to be developed in a manner where these producers have a far better access to buyers as well as suppliers of raw materials and other business services. Excessive dependence by the artisans on traders or ‘direct’ channels, as in Molela for instance, has limited business growth and points to the absence of policy support in enhancing market access.

[Table 3] Major market channels for cluster enterprises

Major market channels for cluster enterprises

It is apparent that for the traditional craft-based clusters located in rural areas market channels have not been adequately developed. Despite variations between the selected clusters here the ‘traders’ have continued to remain the so-called ‘market makers’. That these traders or middlemen extract exorbitant profits by paying low prices to the artisans is well documented. As the market channels are essentially a function of the manner of organization of production, the supply chain there is a definite role for the state to intervene. It would have to work towards identifying and linking the local firms, if possible, to the hitherto inconceivable markets. The Chinese state initiative in what are called ‘market platforms’ (Ding, 2012) to connect remote traditional enterprise clusters to the mainstream domestic and further global markets is an important example in institutional innovation that the Indian rural cluster promotion policies could take cognizance of. Additionally, for the Indian state, an important institutional innovation could be to create systems of generating relevant databases, develop support bases for networking between key cluster or subsector stakeholders and facilitate what are known as business to business (B2B) linkages. This essentially would call for moving beyond the confines of the concerned Ministry of MSME and forge symbiotic association with relevant ministries, specialized financial agencies, research centres, business service providers - public and private. To build up an easily accessible information podium per se would be a first major step in this direction.

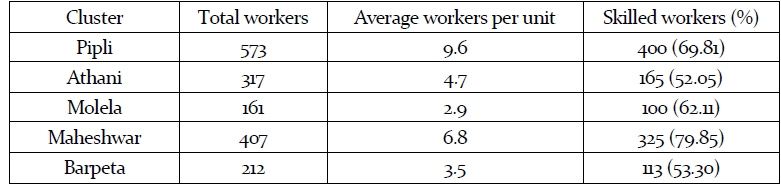

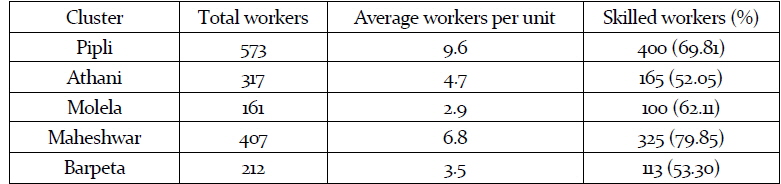

These clusters being largely based upon traditional craft human skill and energy remain the central force behind these forms of business. As shown in Table 4, the proportion of ‘skilled’ workers is high in those crafts (as handlooms, appliqué and terracotta) where skill requirement is intense. That, however, does not reduce the need for the so-called unskilled workers who undertake a variety of activities not always considered skilful by the craftsperson-entrepreneur. Similarly, in case of Maheshwar and Pipli as the processes involved are complex and require discrete engagement, the average size of workers per unit remains much higher as compared to those in Molela and Athani where the number of activities is limited. These numbers, however, conceal the fact that the status of almost all these workers is casual in nature.

[Table 4] Total workers and skilled workers in sample units

Total workers and skilled workers in sample units

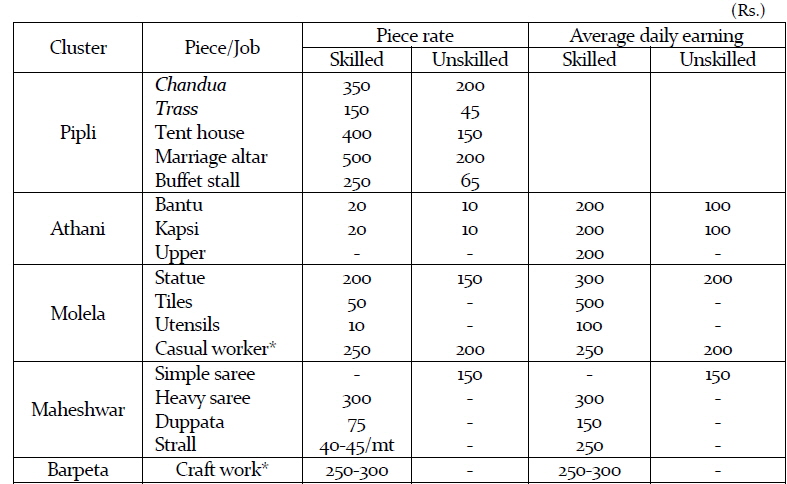

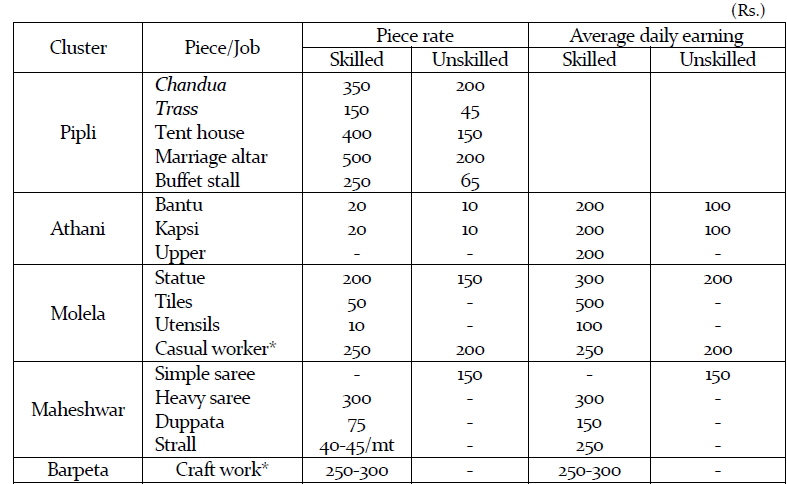

Table 5 corroborates this unambiguously by showing that not only the dominant mode of payment wages is on piece rate basis but also the average daily earnings (for days of work only) is very low, especially, for those activities/jobwork subcontracted to the poor rural dispersed households. This underscores the fact that most such activities have become livelihood-centric in their pursuits as the enterprise is no more than a means barely to survive. That there is hardly any incentive to innovation by these firms is determined by not only the limited market and raw material access but the institutions that perpetuate low income and poor work environment.

[Table 5] Wages and mode of payment

Wages and mode of payment

Even as the skill composition, typically, is determined by the craft in question, once again, the manner of organization of production and distribution assumes centrality. The surveys of the five artisan clusters, unsurprisingly, reveal that casual or informal work has been the sole arrangement of engaging workers, who are mostly paid piece-rate wages. However, in cases where the trader assumes the role of the ‘market maker’ (as in the handloom cluster of Maheshwar or the leather footwear cluster of Athani) and provides advance credit the situation could be theorized to be akin to that of ‘semi-feudalism’ whereby the onus of innovation lies with the trader or subcontractor

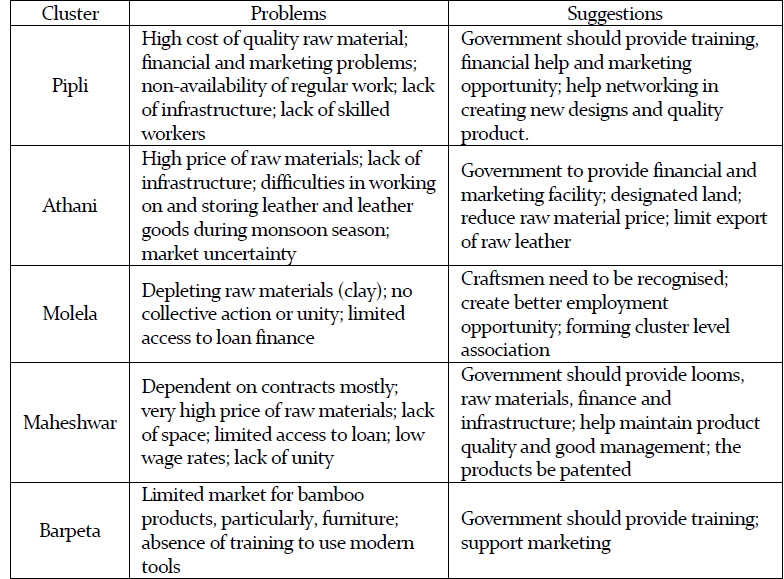

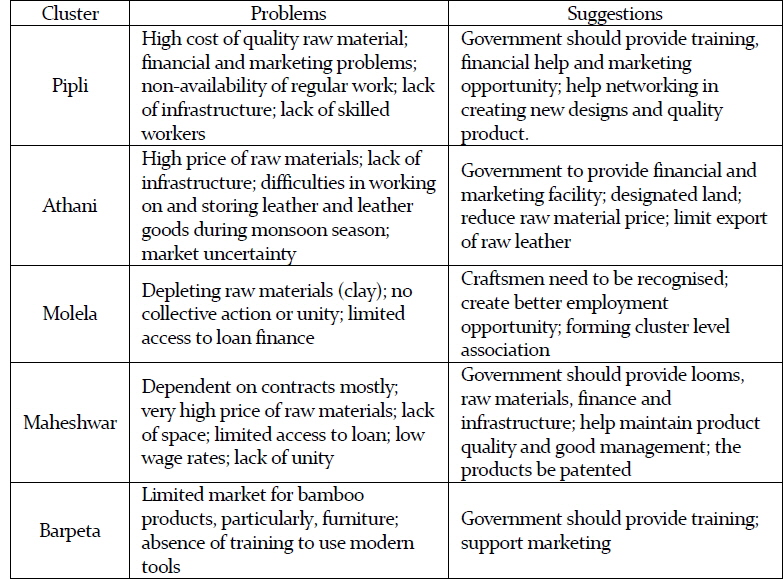

An important issue to address in artisan clusters with varying market reach and potential to introduce innovations would be to learn intently from the artisans themselves, a glimpse of which has been captured in Table 7. The wide variety of suggestions also indicates the huge diversity of the artisan sector which needs serious exploration. Effective and relevant policy suggestions to introduce institutional innovations would have to be drawn upon field reality and not be based upon conventional notions, say, of a bureaucrat, banker or politician, about the subsector or space.

[Table 7] Perceived problems and suggestions by entrepreneurs

Perceived problems and suggestions by entrepreneurs

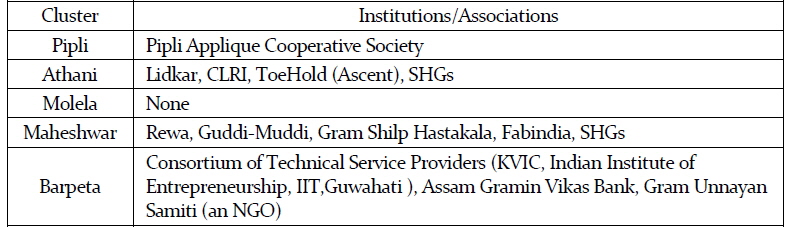

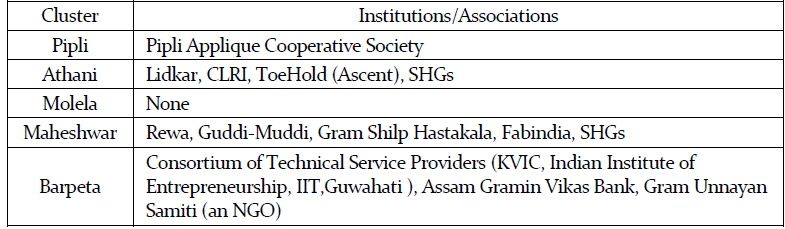

A specific characteristic of clustering of firms has been identified as the potential synergy that promotes collective interests. These institutional arrangements could be either formal or informal as could be through membership in subsectoral associations, informal groupings, SHGs and so on. Such collectives make it easy to access certain indivisible and noncompetitive provisions as basic infrastructure or Geographic Indications (GI) certification at the cluster level. In certain cases, proactive collectives could have a greater role in liaison with the local or central government in obtaining concessions in acquiring a certain technology or license to export. In case of most rural clusters, as with the sample clusters here (with some exception of the Athani cluster), an absence of dynamic collective bodies signals disadvantage to inclusive innovation in a given cluster. Table 6 is indicative of such a situation prevailing in most clusters in rural India.

[Table 6] Formal institutions and associations in the clusters surveyed

Formal institutions and associations in the clusters surveyed

Table 7 compiles the problems facing the select clusters and suggestions for improvement as stated by respondents. The concerns regarding the cost and availability of raw material and skilled workers are strikingly similar across various crafts and spaces. Moreover, as a wayout of the difficulties confronting these clusters there is unanimity in the role of the state in almost all major spheres of business promotion. This remains in complete contrast to a typically held notion regarding cluster development (as in the UNIDO-CDP) that such support should be possible only through the route of participation of or provision by the private sector.

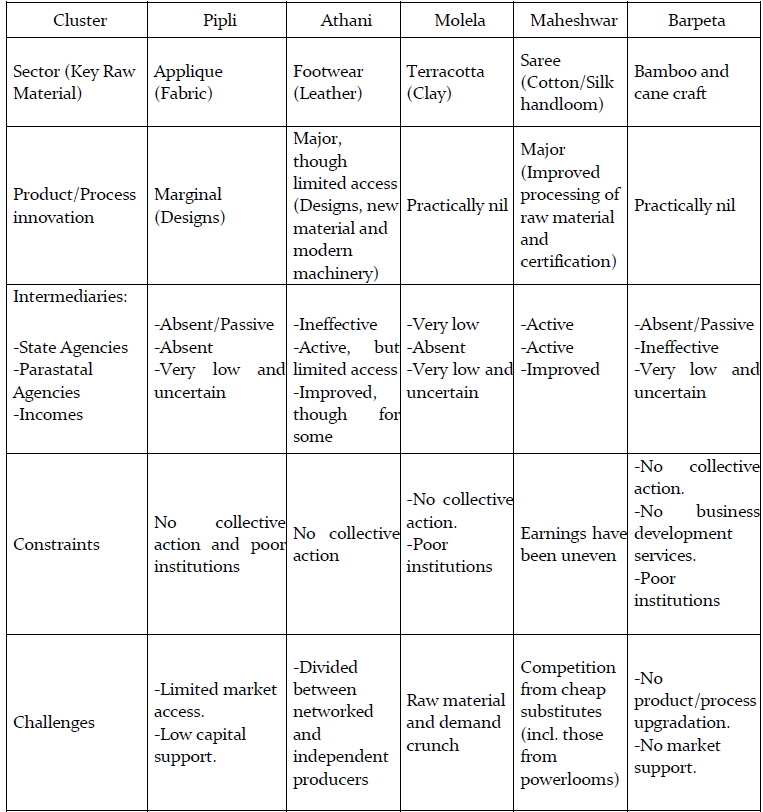

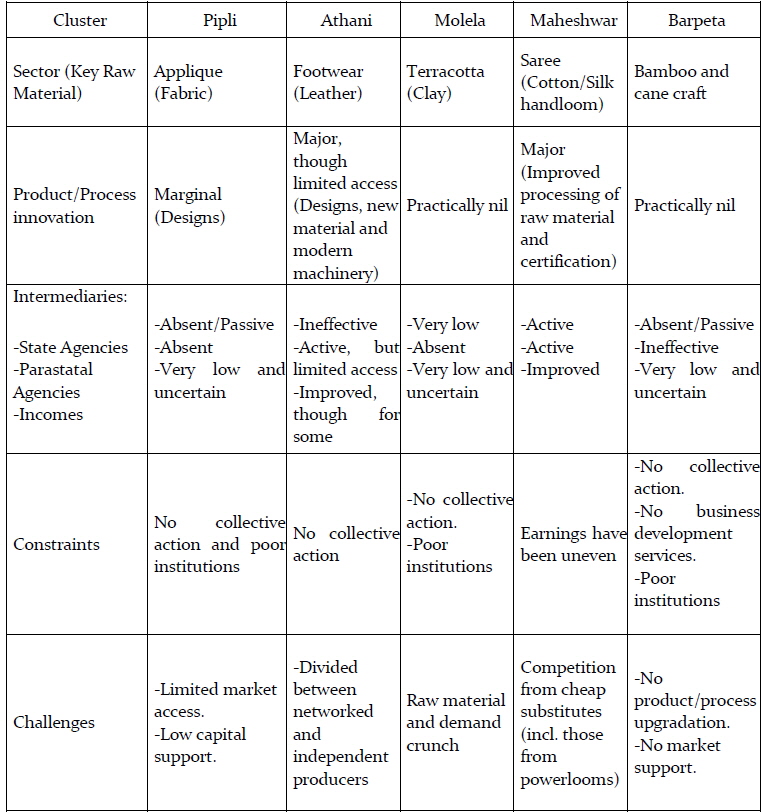

Further, the weak institutional framework supporting cluster activities could act a formidable constraint for innovative ethos to be nurtured in rural or artisan clusters. In fact, as was clear from the field surveys in the five clusters across the country there were several constraints arising out of inadequate or no institutional provision for enhancing access to raw materials, new markets and new technology. Table 8 presents a summary of such institutional limitations across the sample clusters.

Institutional constraints to product/process innovation in the sample clusters in rural India

As one searches for institutional innovations to support product and process innovations, one needs to derive insights from actual cluster dynamics that would reveal the role, depth and complexity of various stakeholders which would influence the innovation ecosystem. As one compares the various agencies and dimensions of institutional constraints in the chosen five craft clusters several questions arise. For instance, while Athani and Maheshwar seem to have introduced some innovations, access to innovations has differed. For instance, in Athani only a limited number of enterprises which joined ToeHold initiative could carry out changes in design, got trained with modern machineries set up through the agency and had an idea about operating in the foreign markets. However, there was a decline in the membership with some complaining about lack of transparency in the actual revenue received by the agency following exports. In Maheshwar, the markets expanded at the national level and with growing demand from discerning buyers product quality, design and scale of production have improved through various relevant innovations in raw material processing, focusing on traditional niche motifs and modifications in the loom technology (undertaken by both local weavers as well as the state department).

While it could be that a wider exposure to the higher level and different types of markets could deeply impact product and process innovations that include developing numerous new designs, use of improvised or imported machinery, better packaging and branding the role of the local cluster association and the state, it remains crucial in staying vigilant to stem unscrupulous practices that could work against the innovative ethos of a cluster. It is important, hence, to explore if the variation in innovativeness and access to innovations are consequent upon the roles played by agencies of the state, local cluster and even external stakeholders? Do market and product characteristics play a role? Are private initiatives more effective compared to state interventions or can a joint effort pave a smooth path for innovations to take shape in the rural craft clusters? These are issues not quite exposited in the complex scenario of the huge craft-based clusters in India.

Rural enterprises, including those in clusters, have dominated the industrial space in India in terms of low-end products, poor income earning options and a near-absence of innovativeness. This has implied limited market access, inadequate organization of production and distancing from sources of formal knowledge. In several cases, there has been a decline in these clusters due to a constellation of factors including non-availability or depletion of raw materials (particularly, forest-based materials like skin, hides, horns, bones, wood, etc. or certain kind of minerals, including clay, stones, etc.); decline in demand for products either due to cheaper and better alternatives available; limited marketing channels; and increasing costs. While in several skill-based clusters activities have become unremunerative, modernity has also kept the next generation away from these essentially traditional and unattractive occupations.

Beyond these widely acknowledged constraints, there has been significant institution deficit, by which we refer to exclusion - unintended or otherwise - as the final outcome. Whether it relates to access to loan finance or technology support or linking to markets, the formal institutions (public or private) have been distanced by informality that characterizes most rural enterprises and clusters. The state, in particular, has pursued generally uninnovative strategies through mouthful of policy proclamations and rarely has reviewed why its several schemes never benefited or even reached the needy artisan. An obsession with a sectoral approach, following the global stylized interventions to cluster development, has essentially defeated the very purpose by negating the importance of space - importantly, if it is non-urban. Moreover, there is little learning from the meaningful experiments in rural enterprise promotion in Asia and elsewhere.

As the case studies of rural clusters indicate, extant institutions lack coordination, progressive vision and a feel for the context within which these clusters function. The continuing dominant policy thinking has been that the artifact-centric technological dynamism is a precondition for transforming the ‘production’ clusters into ‘innovation’ clusters. These are, as had been pointed out at least a decade ago (Das, 2005a), narrow sectoral approaches to cluster development that leave no scope for broader thinking, that is, to construe rural and traditional clusters as business propositions which would seriously require a holistic approach to take recourse to the existing institutions and also to create anew to facilitate craft promotion and livelihood options. It is yet to be appreciated that the institution-centric innovation system fosters the firms’ ability to upgrade both in terms of attaining higher degree of competence and conducting business in a pragmatic and cooperative manner. The OVOP-OTOP initiatives as in some Asian economies provide helpful clues in this direction.

The rapid advancement in the electronics and telecommunications technology, infrastructure and spread even in rural areas has been referred to as a significant opportunity for traditional craft clusters to enhance their business using these technological advantages. For instance, there has been a spectacular rise in the use of mobile phones and internet (although the speed of data transfer still remains slow and signal poor) in rural areas and small towns in India and several private initiatives (often through nongovernmental organisations) and even government departments have been helping promotion and sell of craft products through such arrangements as e-commerce. Similarly, several institutions, for example, National Bank for Agriculture and Rural Development, Development Commissioner (Handicrafts), Ministry of Textiles, Securities and Exchange Board of India and Khadi and Village Industries Commission have come up with schemes of providing business development services, venture capital, marketing support and so on. While there have been sporadic instances of notable performance of rural clusters through these various interventions no systematic effort has been undertaken even to have a comprehensive database on the craft clusters in India that would capture their key characteristics, challenges and potential. Transparency in participation and terms of business contracts are also other issues that remain to be addressed across the sector.

It is important, hence, to assess the gravity of regional and institutional infirmities while planning for rural clusters to progress. The larger challenge that still remains, and not quite comprehensively addressed in policy and academic engagements, is that of the nature and extent of informality, which impinges upon the possibility of rural enterprises/clusters availing formal support and also acts as a definite disincentive to innovate by firms. Rural enterprise clusters must not be allowed to disintegrate due to institutional apathy nor the artisans be forced into a situation where business and craft barely provide for their subsistence but not a brighter future for the next generation.