The twentieth century witnessed a dramatic increase in global population, increased use of natural resources and rapid industrial expansion resulting from technological advancement (McAlister, Ferrell and Ferrell, 2005). Although this industrial activity resulted in improved standards of living, it came at a cost to the environment: natural systems and habitats, being especially vulnerable to human activity because of limited adaptive capacity, have undergone significant damage (Ambec and Lanoie, 2008); plant and animal species, along with wildlife habitats, are disappearing at an accelerated rate; and water has become a critical resource in some parts of the world (McAlister et al., 2005). Recurrent smog alerts, acid rain, holes in the ozone layer, and global warming are other examples of the effects of uncontrolled industrial activity on the environment (Ambec and Lanoie, 2008).

As society has become more aware of these negative impacts, it has applied increasingly stronger pressure on organizations for improved environmental performance and this is well documented in management literature (Angell and Klassen, 1999; Banerjee, 2001; Fineman and Clarke, 1996; Ramanathan et al., 2014). Typically, expenditure on improving environmental performance was viewed by firms as costs that correlate negatively with returns. However, a positive link between environmental performance and financial performance would ‘license companies to pursue the good-even by incurring additional costs-in order to enhance their bottom line and at the same time contribute more broadly to the well-being of society,’ (Margolis et al., 2007: 4). While profitability may not be the only reason why firms will or should consider their social and environmental performance, it has become the most influential (Vogel, 2005). Investigation of this link has been the subject of several research studies in the past. However, the available evidence is inconclusive; some studies found a positive link, some found a negative link, while others found no link at all. Given such inconclusive evidence, several studies have attempted to determine how this link is affected by various related characteristics of a firm. For example, the mediating role of training has been established by Sarkis et al. (2010). The moderating role of complexity, uncertainty and munificence has been studied by Rueda-Manzanares et al. (2008). Innovation plays a moderating role as shown by Eiadat et al. (2008), Hull and Rothenburg (2008), Jaffe and Palmer (1997), Montabon et al. (2007) and Triebswetter and Wackerbauer (2008).

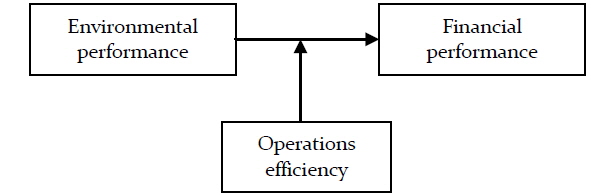

Operations efficiency plays an important role in a firm’s ability to undertake waste minimization and in developing environment friendly activities (Doh et al., 2009). A good relationship between lean manufacturing and sustainability has been observed by Kleindorfer et al. (2005) and Toffel and Lee (2009). Pagell and Gobeli (2009) have observed close relationship between environmental performance and operational performance. Triebswetter and Hitchens (2005) have found a positive correlation between the number of environmental initiatives and the productivity levels of firms. These observations favor the view that firms that are proactive in improving their operations efficiency and invest in lean programs would perform better on environmental indices. Since the objective of many lean-related activities in firms is to enhance their financial bottom-line (Berman et al., 1999), firms that emphasize operations efficiency should be able to achieve better financial performance. The literature provides some evidence pointing to a moderating role for operations efficiency on the relationship between environmental performance (EP) and financial performance (FP) but this moderating relationship has not yet been tested empirically. This paper attempts to fill this gap by studying data from three independent data sets.

The rest of the paper is organized as follows. We review the literature linking environmental and financial performance in the next section. We draw on the resource-based-view as a theoretical basis to argue for the moderating role of operations efficiency on the link between environmental performance and financial performance. Our hypothesis is developed in this section. Section 3 discusses the data and methodology of our study. We combine two different secondary data sets to test our hypothesis: perception based scores on Britain’s Most Admired Companies (BMAC) and the Financial Analysis Made Easy (FAME) that contains some financial performance measures of these companies. Measures of environmental performance, financial performance, operations efficiency, and other control variables from our data sets are discussed in this section. Details of our regression analyses and results are presented in Section 4. Our results are discussed in Section 5 along with managerial implications. The last section discusses conclusions of our study.

1. The Resource-Based View of a Firm

The resource-based view (RBV) of a firm tries to understand how a firm can exploit its internal resources for sustained competitive advantage. It has rich reputation as the underlying theoretical principle linking environmental performance (EP) with financial performance (FP) (e.g., Russo and Fouts, 1997; Judge and Douglas, 1998; Klassen and Whybark, 1999; Hart, 1995; Hart and Ahuja, 1996; Sarkis et al., 2010). This theoretical paradigm seeks to explain firm behavior and the subsequent outcomes – financial and otherwise – not in terms of factors outside the firm, such as market structure or the degree to which the industry is characterized by fixed costs, but rather in terms of factors internal to the firm i.e., its resources (Barney 1991). In order to deliver sustained competitive advantage, these resources must be “valuable, rare, imperfectly imitable, and not substitutable. These resources and capabilities can be viewed as bundles of tangible and intangible assets, including a firm’s management skills, its organizational processes and routines, and the information and knowledge it controls” (Barney, Wright and Ketchen Jr., 2001:625; González-Benito and González-Benito, 2005; Rueda-Manzanares et al., 2008). The RBV recognizes that the basis for the competitive advantage of an organization lies primarily in the application of the bundle of valuable resources at its disposal (Rumelt, 1984:557-558; Wernerfelt, 1984:172).

RBV helps in understanding the proactive development of efficient technologies by environmentally active firms. Firms with proactive environmental performance generally accumulate valuable know-how on pollution prevention in the long run. This know-how is inimitable and will be the source for competitive advantage to the firm. Thus RBV generally supports the positive link between EP and FP.

2. Direct Relationships between Environmental Performance and Financial Performance

In the following sections, we first review studies that explored the existence of a direct relationship between environmental performance and financial performance, and then review those that made a case for more complex possibilities.

2.1 Evidence for a Direct Relationship: Positive and Negative

A positive relationship between environmental performance and financial performance has been reported by Hart and Ahuja (1996), Waddock and Graves (1997), Russo and Fouts (1997), Balabanis et al., (1998), Orlitzky (2001), Margolis and Walsh (2003), Salama (2005), Margolis et al., (2007), Montabon et al (2007), Callan and Thomas (2009) and Peloza (2009). Support for a positive link has also been highlighted in case studies (Rugman and Verbeke, 2000; Porter and van der Linde, 1995; Marshall and Brown, 2003; Preston, 2001) as well. As mentioned earlier, the RBV generally predicts positive association between EP and FP.

A negative relationship was reported by Cordeiro and Sarkis (1997), Konar and Cohen (2001), Moore (2001), Sarkis and Cordeiro (2001), and Brammer et al., (2006), who argue that firms trying to enhance social/environmental performance draw resources and management effort away from core areas of the business, resulting in lower profits.

Other researchers have investigated the direction of causality in this relationship. The so called ‘virtuous circle’ in which environmental performance impacts financial performance and vice versa is supported by Hart and Ahuja (1996), Waddock and Graves (1997), Schaltegger and Synnestvedt (2002), Orlitzky et al., (2003), and Vogel (2005). Peloza (2009) has found that financial performance has more impact on environmental performance than environmental performance has on financial performance.

A relationship between environmental performance and economic performance might be expected since both require the use of strategic resources required for competitiveness (Klassen and Whybark, 1999) such as continuous improvement, stakeholder management (Hart, 1995), physical assets and technology, organizational culture, inter-functional coordination, and other intangible resources (Russo and Fouts, 1997). Environmental regulation might create a link between environmental and economic performance in situations where regulatory tools give strong economic incentives for improvements in environmental performance (Schaltegger and Synnestvedt, 2002).

Environmental Performance can provide a firm with economic benefits through increased sales, reduced costs and potential mitigation of harmful events (Peloza, 2006). Since pollution levels are increasingly critical, any environmental incident may tarnish a firm’s reputation in addition to subjecting it to substantial legal costs and fines (Eiadat et al., 2008) which can have significant impacts on financial performance. As a firm makes strategic investments that reduce emissions and pollution, it mitigates its risk of litigation (Sharfman and Fernando, 2008). This effect is referred to as an ‘insurance effect’ for firms that engage in environmental and social performance (Godfrey et al., 2009).

In general, it is expected that there could be both positive and negative impacts on performance and competitiveness as a result of improvements in environmental performance which require changes in processes, production methods, handling of by-products, product innovation, and pollution prevention and control (Rothwell, 1992; Hitchens, 1999; Hitchens et al., 2005). These improvements are likely to represent additional costs in the short term but could provide competitive advantage for the firm in the long term. The extent to which environmental performance would result in an improvement in economic performance depends on factors such as consumers’ willingness to pay for environmentally friendly goods, the nature of environmental and health regulations in a country, stakeholder pressure in different industries, intensity of competition within the market and the level of technological development (Schaltegger and Synnestvedt, 2002).

2.2 No Evidence for a Relationship

A neutral relationship or little evidence for a direct relationship has been reported by Aras et al., (2010), Jaffe et al., (1995), Johnson and Greening (1999), Berman et al., (1999), McWilliams and Siegel (1997, 2000), Thornton et al., (2003), Elsayed and Paton (2005) and Vogel (2005).

Margolis et al (2007) have suggested that financial performance would be an unlikely rationale for pursuing environmental performance since some other areas of the organizations may be able to result in more direct and significant financial impacts. Hitchens et al., (2005) have found that improved environmental performance is not associated with a decrease in financial performance. This suggests that the allocation of resources to improve environmental performance may be a necessity that is not subject to performance constraints (Johnson and Greening, 1999) and that firms can succeed competitively without facing favorable environmental costs (Hitchens, 1999).

Vogel (2005) has found no evidence that environmentally responsible behavior makes firms more profitable or that it makes them less profitable. Thornton et al (2003) have also found no evidence that firms gained significant competitive advantage by adopting innovative environmental technologies or products even though the implementation of these technologies led to improved environmental performance. Margolis and Walsh (2003) have stated that there is little evidence that environmental performance destroys value, injures shareholders in a significant way, or damages the wealth-creating capacity of firms. Triebswetter and Hitchens (2005) have found that environmental performance neither led to an improvement in nor to a loss in the overall competitiveness of firms. These studies suggest that environmental performance may not have a direct impact on the financial performance of a firm.

Thus, based on the literature so far, we have found mixed evidence on the relationship between environmental performance and financial performance. However, we tentatively posit a significant positive relationship in the form of the following hypothesis.

H1 Environmental performance is positively related to financial performance.

3. The Case for Indirect Effects

Vogel (2005), while finding no evidence between EP and FP, has further suggested that the relationship might be indirect and that EP would yield benefits for firms in specific circumstances. For example, good environmental actions are said to be profitable because good management would usually lead to such results (Schuler and Cording, 2006; Peloza and Papania, 2008). Wagner and Schaltegger (2004) have found that for firms with shareholder-value-oriented strategies the relationship between environmental performance and economic performance is more positive than for firms without such a strategy. Lopez-Gamero et al., (2009) have also found that the effect of environmental performance on firm performance is indirect and could vary depending on the sector considered. Elsayed and Paton (2009) have found that the influence of corporate financial performance on corporate environmental policy varied with firm life cycle.

Peloza (2009) has suggested that the most important direction for future research lies in understanding, through examination, the indirect processes between environmental performance and financial performance. Two reasons were given for this: for understanding how environmental performance creates business value; and for developing leading indicators to assess this value early in the process.

One emerging view is that previous studies on the environmental-financial performance relationship have not taken into account the total benefit of environmental performance which includes increased revenues through innovative products, improved operations efficiency and the prevention of environmental disasters which otherwise could have negative effects on firm performance (Peloza, 2006; Yu and Ramanathan, 2015). This insurance effect is beneficial to firms through direct and indirect relationships (Sharfman and Fernando, 2008). For example, risk management through environmental performance can lead to reductions in cost of capital and a reduced cost basis leading to larger profits for any given income level (Sharfman and Fernando, 2008).

In this paper, we use the resource-based-view to argue that firms with high operations efficiency should exhibit better links between environmental and financial performance.

A firm that is proactive in improving its operations efficiency will be able to develop capabilities that cannot be easily imitated by competitors. This often involves the redesign of the firm’s production processes or service delivery processes with new technologies being developed or acquired to achieve maximum efficiency. As mentioned earlier, the RBV helps in understanding the proactive development of newer efficient technologies by firms wishing to improve their operations efficiency. Even if the technologies are acquired (which may not directly result in competitive advantage since the same technologies will be available to competitors as well), the RBV would help describe the efforts of operationally efficient firms in their ability to adapt these technologies for operational improvements and to continuously find ways to improve efficiency (Russo and Fouts, 1997). These efforts are unique to operationally efficient firms and are not easily imitable.

Environmental performance indicators such as waste minimization are consistent with process efficiency initiatives such as lean manufacturing and six-sigma quality improvement programs (Melnyk et al., 2003; Toffel and Lee, 2009). Thus an organization with high operations efficiency is likely to reduce waste more efficiently when compared to another with low operations efficiency. Lean principles such as eliminating waste, involving all stakeholders, and continuous improvement (Slack et al., 2009) are equally applicable in improving environmental performance. The higher the operations efficiency of a firm, the lower will be its waste and scrap rates (Porter and van der Linde, 1995).

There are few studies that explored the role of operations efficiency on the link between environmental performance and financial performance. Zhu and Sarkis (2004) have shown that operational practices such as quality management and ‘just-in-time’ moderate the impact of supply-chain-management practices on performance. Samson and Terziovski (1999) have shown that quality management practices were closely associated with the performance of manufacturing firms in Australia and New Zealand. Similar observations have been made by Kaynak (2003) in the US. Cohen et al. (1997) have suggested that firms with more efficient manufacturing processes also pollute less. This improves not only resource efficiency, but also has a payoff in terms of the market’s perception of the risk profile of the firm (Sharfman and Fernando, 2008), which might help explain why better environmental performers tend to be better financial performers. The development of environmentally friendly manufacturing systems can provide firms with a means of improving efficiency while simultaneously minimizing the costs associated with environmental compliance (Florida, 1996; Berman et al., 1999) and driving down operating costs (Berman et al., 1999).

Environmentally responsive firms generally experience enhanced efficiency and lower operating costs (Russo and Fouts, 1997; Shrivastava, 1995). Environmental performance, through improved operations efficiency, can also reduce the likelihood of accidents (Henriques and Sadorsky, 1996), which could help avoid serious problems for management. Such extreme environmental events usually require significant cash outflows to deal with compensation and cleanup costs, making firms more vulnerable to bankruptcy and other adverse business developments which could reduce profitability, impair the firm’s reputation or reduce the value of its asset base (Sharfman and Fernando, 2008).

There is limited empirical evidence on the influence of operations efficiency on environmental performance. Berman et al. (1999) have shown that firms that possess cost-leadership qualities (measured via cost efficiency, defined as the ratio of the cost of goods sold to total sales, with lower values indicating higher operations efficiency) achieve better financial performance. Using case studies, Triebswetter and Hitchens (2005) have found that high productivity plants have implemented more number of environmental initiatives than low productivity firms. More recently, Doh et al. (2009) have found that environmentally “more active” firms (that are added to a social index) achieve superior operations performance compared to environmentally “less active” firms (that are deleted from the social index). However, empirical studies to understand the moderating influence of operations efficiency are missing in the literature and our study fills this gap.

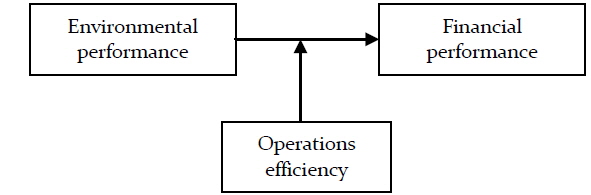

We expect that firms with better operations efficiency will be able to achieve better environmental performance and hence better financial performance, highlighting the moderating effect of operations efficiency. Our second hypothesis is based on this moderating role, illustrated in Figure 1.

H2 Operations efficiency positively moderates the relationship between environmental performance and financial performance; firms with higher levels of operations efficiency will be able to register stronger links between environmental performance and financial performance.

To summarize this section, we have explained how RBV theory could provide the theoretical background for this study, and explained the literature linking environmental performance and financial performance of firms. We have shown that there is no conclusive evidence for this relationship and hence argued for more complex links. Finally, we have argued that operations efficiency could help understand the complex links, and hypothesized a moderating role of operations efficiency. In the next section, we discuss the variables and data for validating the above hypotheses.

III. Measurement of Variables and Data Sources

1.1 Measuring Environmental Performance

The construct of social/environmental performance is associated with the following four broad measurement strategies: (a) disclosures; (b) reputation ratings; (c) social audits, processes, and observable outcomes; and (d) managerial principles and values (Orlitzky et al., 2003).

Environmental performance has been measured with independent third-party ratings such as Britain’s most admired companies ratings and the Kinder Lyderberg Domini (KLD) ratings (Salama, 2005; Elsayed and Paton, 2005; Waddock and Graves, 1997; Hull and Rothenburg, 2008; McWilliams and Siegel, 2000; Godfrey et al., 1999; Sharfman and Fernando, 2008), pollution control indices e.g. Toxic Release Inventory (TRI) (Hart and Ahuja, 1996; Klassen and Whybark, 1999; Sharfman and Fernando, 2008), and the presence of an environmental management plan (Henriques and Sadorsky, 1996). Regulatory compliance expenditures, pollution control expenditures and pollution abatement costs (Brunnermeier and Cohen, 2003; Jaffe and Palmer, 1997) and standards, charges and other instruments (Hitchens, 1999) have been used as proxies for environmental regulation. Thornton et al. (2003) used measures of water pollutants (biochemical oxygen demand, total suspended solids, absorbable organic halides, chemical spill incidents) as measures of environmental performance in their study on pulp manufacturing mills. All these measures have been subjected to criticism and no consensus has emerged yet as to how either environmental performance can or should be measured (Vogel, 2005).

The most frequently used measures are reputational (perception) measures such as the Fortune reputation ratings and the indices of KLD Research and Analytics in the US. In the UK, similar ratings are published by the Management Today magazine in their annual BMAC ratings. Ilinitch et al. (1998) have suggested that, while such ratings may simplify cross-company comparison, they are insufficient to gauge a company's environmental performance with confidence. Another criticism of these ratings is that the raw scores appear to be heavily influenced by a company’s previous financial and environmental performance, which means that any relationship between it and profitability might be tautological (Vogel, 2005).

Despite these criticisms, they are more readily available and widely used. Chatterji et al. (2009) found that KLD ratings do a reasonable job of aggregating past environmental performance but they do not predict subsequent environmental outcomes.

For this study, the community and environmental responsibility scores from the BMAC survey (BMAC, 2008) is used as a measure of environmental performance. Thus, in this research, environmental performance is measured by performance in terms of community and environmental responsibility.

1.2 Measuring Financial Performance

The three broad subdivisions of measures of financial performance previously used are market-based (investor returns), accounting-based (accounting returns), and perceptual (survey) measures (Orlitzky et al., 2003; Peloza, 2009).

Agle et al. (1999) used Return on Assets (ROA) and Return on Equity (ROE) as measures of financial performance, Brammer and Millington (2008) used stock performance as a measure of financial performance and Cordeiro and Sarkis (1997) used Industry security analyst earnings forecasts of future accounting performance as a measure of financial performance. Berman et al. (1999) have measured financial performance using ROA (operating income divided by total assets).

Johnson and Greening (1999) have measured firm performance using two-year averages of ROA, ROE, and Return on Sales (ROS) to reduce the impact of possible accounting inconsistencies. Firm performance has also been measured using sales growth, market share and return on investment (Eiadat et al, 2008) and profitability (ratio of pre-tax profits to total assets) (Brammer and Millington, 2008).

As sustained growth in financial performance is a primary goal for most managers, accounting-based measures are frequently used in evaluating the performance of management (Balanabis et al., 1998). They are often used over the long term or to value initiatives that are expected to generate value in the short term (Peloza, 2009).

For this study, based on previous studies (Agle et al., 1999; Berman et al., 1999; Johnson and Greening, 1999), we have used ROA to represent financial performance. ROA measures how efficiently a firm uses its assets to generate value, and seems appropriate because it represents the revenue received by a firm with respect to the total set of resources or assets, under its control.

1.3 Measuring Operations Efficiency

Berman et al. (1999) have argued that cost efficiency (the ratio of cost of goods sold to total sales) could be used to represent the operations efficiency of a firm. It is expected that a small cost efficiency value would indicate better operations efficiency since the firm spends less to produce its products. For this study, cost efficiency is calculated as the ratio of cost-of-sales to turnover. However, we prefer to use the term “cost-to-turnover ratio” instead of “cost efficiency,” because higher efficiencies are generally associated with better performances but firms with higher cost-to-turnover-ratios indicate lower levels of operations efficiency.

1.4 Control Variables

When financial performance is the dependent variable of concern, it is important to control for other factors that also have significant impact on performance (Florida, 1996; Balanabis et al., 1998; Capon et al., 1990; Berman et al., 1999; Vogel, 2005). This will ensure that the model adequately reflects operating environment of a firm and that reliable results are obtained (McWilliams and Siegel, 2000). Past research on the environmental-financial performance link (Capon et al., 1990; Hart and Ahuja, 1996; Waddock and Graves, 1997; Johnson and Greening, 1999; McWilliams and Siegel, 2000; Orlitzky, 2001; Elsayed and Paton, 2005; Salama, 2005; Peloza, 2006, 2009; Hull and Rothenberg, 2008; Brammer and Millington, 2008; Sharfman and Fernando, 2008) have identified and controlled for the effects of the following variables: quality of management, capital investment, size, risk or resource leverage, industry effects, firm age and R&D intensity.

There may be a reciprocal relationship between the level of

It is important to include

Thus, the control variables used in this study are risk, total assets, quality of management, number of employees, capital intensity and industry.

Since the study requires different kinds of data that are not available in a single database, we obtained our data from two different sources – (1) Britain’s most admired companies (BMAC) database, and (2) the Financial Analysis Made Easy (FAME) database.

2.1 Britain’s Most Admired Companies Ratings

Britain’s Most Admired Companies is a yearly survey conducted on publicly listed British-owned companies and is published at the end of each year by

Scores are assigned to each firm between 0 and 10 for each criterion. The values are then aggregated to give the final score for each firm in each criterion. The scores in the nine criteria for a company are then added up to give its final score and hence the rating. The BMAC score provides the most detailed and consistent rating of firms in the UK in terms of the nine criteria covered, and has been used in previous studies (e.g., Salama, 2005; Elsayed and Paton, 2005). We have used survey results for the year 2008 (reported in December 2008) (BMAC, 2008) in this study.

2.2 Financial AnalysisMade Easy Database

Financial data (Total assets, number of employees, ROA, turnover, cost of sales, long-term debt) have been obtained from the FAME database for the 240 companies for the year 2007. It was decided to collect data for 2007 because the BMAC survey published in December 2008 was carried out during the year 2008. Most of the managers that responded to the survey must have based their judgments on their experiences in 2007. However, all the required financial data were not available for some companies, and the sample size for the analyses discussed in the next section is much below 240.

To summarise this section, we have discussed the variables (dependent variable, independent variables and control variables) for this study to help verify the hypotheses developed in Section 2. We further discussed our data sources (BMAC database and FAME database) for collecting data on these variables. In the next section, we present the analysis and discuss the results.

The hypotheses developed were tested using hierarchical regression because of the need to assess the marginal predictive contribution of the theoretical variables over and above that of the control variables. The moderating impact of operations efficiency has been tested using moderated regression analysis (Hair et al., 2006; Li and Atuahene-Gima, 2001; Miles and Shelvin, 2001; Zhu and Sarkis, 2004). The analysis has been performed using SPSS (v16.0) statistical software.

For the regression discussed below, we first carried out the usual tests to check whether the assumptions of regression are valid for the data. We have tested for normality assumption of the error terms and checked for multi-collinearity and heteroskedasticity. We have verified and found that all assumptions for regression are satisfied. There was evidence of multi-collinearity with some variable-inflation factors (VIF) above the threshold of 5 (Hair et al., 2006) in our moderated regression analysis. To overcome this problem we employed an orthogonalizing procedure, which is based on replacing the interaction term with related residuals (Saville and Wood, 1991). This procedure will be explained during our discussion on moderated regression analysis later in this section.

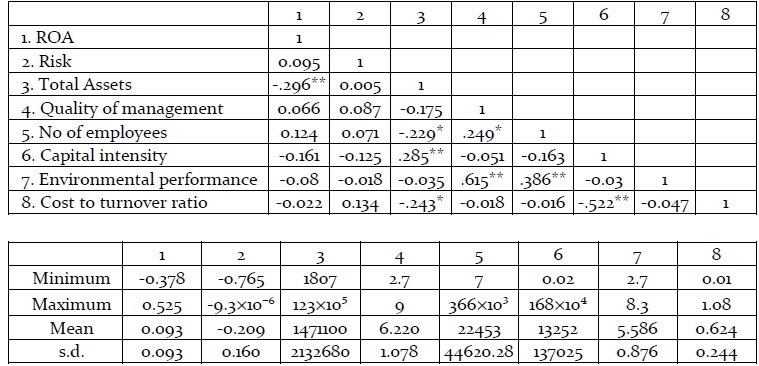

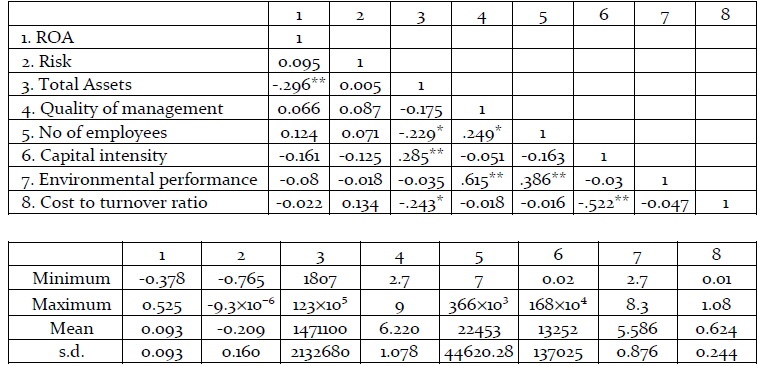

A total of 136 companies remained in the sample after the exclusion of firms for which complete data were not available. The descriptive statistics and correlation matrices for this sample are presented in Table 1.

[Table 1] Descriptive statistics and correlation matrix for all variables used

Descriptive statistics and correlation matrix for all variables used

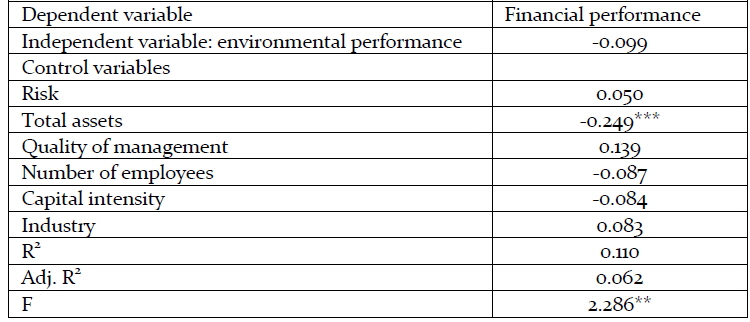

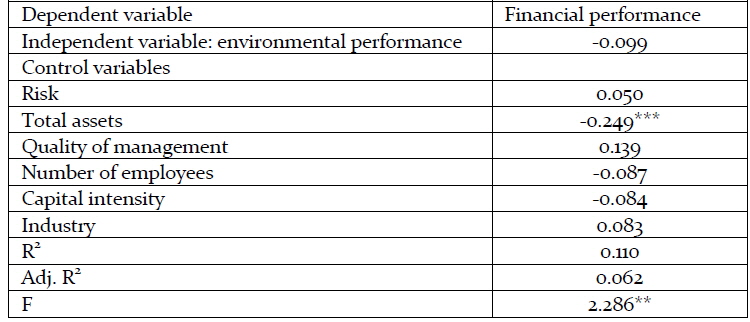

The result of the regression analysis examining the direct impact of environmental performance on financial performance is presented in Table 2.

Regression results

Table 2 presents the regression results in which financial performance is the dependent variable and environmental performance is the independent variable while controlling for other significant factors. The results show that there is no evidence that environmental performance has a direct impact on financial performance. Thus, this finding does not support our first hypothesis.

To verify the moderating influence of operations efficiency on the relationship between environmental performance and financial performance, we carried out a moderated regression analysis (Hair et al., 2006; Li and Atuahene-Gima, 2001; Zhu and Sarkis, 2004). In a moderated regression, a dependent variable is regressed on independent variables, moderator variables, and product-terms of the independent and the moderator variables (Hair et al., 2006). The impact of the moderator variable is assessed using a two stage regression (Li and Atuahene-Gima, 2001). In the first stage, the dependent variable is regressed with the independent variables, moderator variables and control variables (if any). In the second stage, a product-term (independent × moderator variable) is added. The impact of the moderator is assessed based on the improvement in R2 in the second stage regression over the first stage. If this change is statistically significant, then a significant moderator effect is predicted (Hair et al., 2006). Hair et al., (2006) further suggest that only the incremental effect is assessed for checking the significance of the moderation effect and not the significance of individual variables are considered relevant.

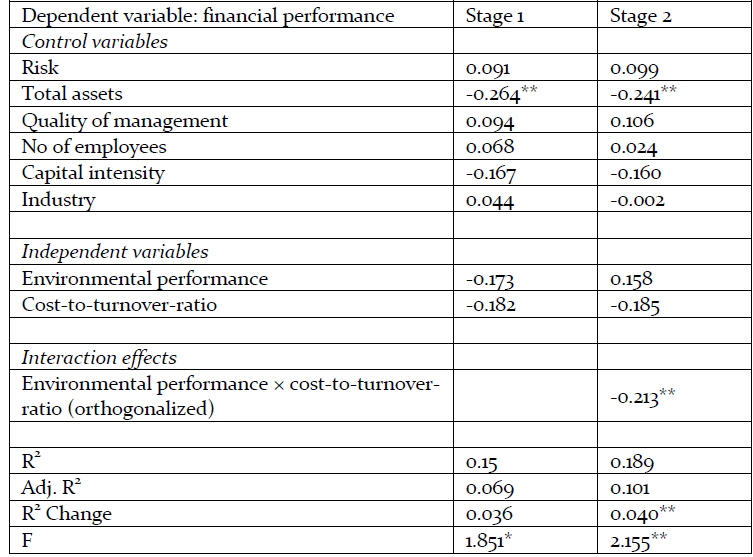

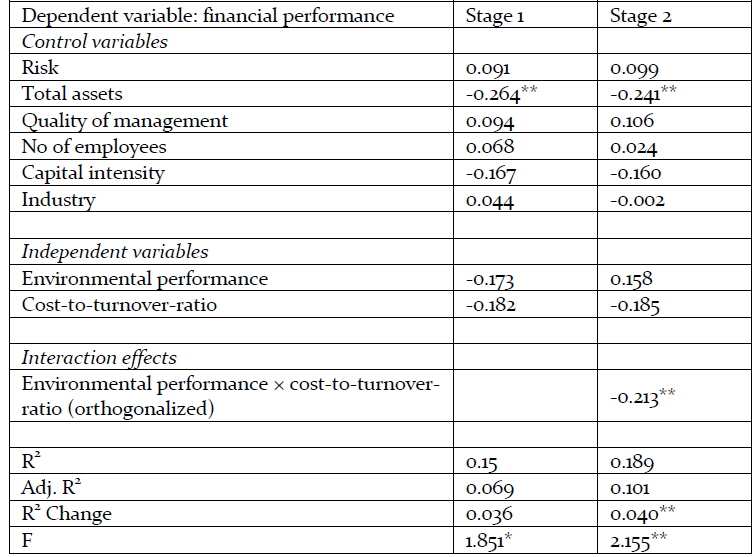

The results of the analysis to test the moderating effect of operations efficiency on the relationship between environmental performance and financial performance are presented in Table 3. As mentioned earlier, moderated regression analysis involves the use of a product-term of the independent variable (environmental performance) and the moderator variable (cost-to-turnover ratio) in Stage 2. However, as in many moderated regression analyses in the literature (e.g., Brock et al., 2006), introduction of the product-term increased the corresponding variable inflation factor (VIF), to 66, which is much above the recommended cut-off value of 5 or 10. Hence, we orthogonalized the product-term using the procedure suggested by Saville and Wood (1991). This procedure involves first running a simple regression with the product-term as the dependent variable and environmental performance and cost-to-turnover ratio as the independent variables. The unstandardized residual of this regression was used as a “true” measure of the interaction, replacing the product-term in the moderated regression. Inclusion of the orthogonalized product-term reduced the VIF value to 1.148, which is well within the acceptable limits.

Regression results

The results presented in Table 3 show that the coefficient of the product-term (environmental performance × cost-to-turnover ratio) is negative and significant (p=0.048). This confirms the moderating impact and indicates that the impact of environmental performance on financial performance is stronger in firms with low cost-to-turnover ratio. Since lower cost-to-turnover ratios indicate higher operations efficiencies, these results support our second hypothesis that environmental performance affects financial performance more positively in the case of firms with higher operations efficiency.

This study has responded to calls in past research to utilize more complex models (Peloza, 2009) and to investigate more complex possibilities when analyzing the relationship between environmental performance and financial performance. Peloza (2009) suggested that researchers should focus less on whether environmental performance has a direct impact on financial performance and concentrate on investigating the mechanisms or routes through which environmental performance can lead to financial performance. Our study is an attempt in this direction. It has done this by investigating the impact of operations efficiency on the environmental performance-financial performance link.

This study has used hierarchical regression to examine the relationships between these variables and combined two different data sets (perception based scores and a financial database) in the UK. Our study found that operations efficiency strongly moderates the relationship between environmental performance and financial performance. It was observed that for firms with higher levels of operations efficiency, improvements in environmental performance had a stronger impact on financial performance. Thus we found evidence that firms that achieve better cost reduction by investing in operations improvement initiatives such as lean manufacturing, ISO 9000 certifications, and six-sigma can also improve their environmental performance from such improvements, and that these improvements lead to better financial performance.

The result of this study agrees with the propositions made in the win-win hypothesis (Porter and van der Linde, 1995), which suggests that improvements in environmental performance lead to a reduction in costs and to higher profits for these firms. Doh et al. (2009) found that improved operating efficiency co-varied with improved environmental performance, which also supports our findings.

We believe that our results support the RBV as a theoretical paradigm. A firm active in improving its operations efficiency will undertake conscious and systemic efforts in improving the efficiency of its production and service delivery processes. These efforts accumulate over time to a wealth of knowledge and translate into internal competitive advantage, which cannot be easily imitated by competitors (Russo & Fouts, 1997). These efforts often result in waste minimization and hence improve the environmental performance of the firm. Hence, for operationally efficient firms, investments in environmental performance will generate better financial performance compared to other, operationally inefficient firms. Our results support the strategic need for harnessing internal resources to meet external demands (Collis and Montgomery, 1995).

In summary, our study has extended the applicability of the resource-based view of the firm. RBV has already been applied to understand the links between environmental performance and corporate performance (e.g., Russo & Fouts, 1997; Hart, 1995), but our study applies the RBV to understanding the more complex role of operations efficiency (which is an internal capability of a firm). We believe that our study highlights the greater breadth of the applicability of the RBV to understand the role of internal capabilities and processes in giving competitive edge to firms.

Our results provide vital clues to being innovative in meeting the growing environmental demands on firms. A number of recent developments, including climate change concerns and environmental pollution, are forcing firms to develop innovative ways to deal with environmental concerns. Perhaps one avenue open to managers is to use their existing capabilities, resources and knowledge in improving their operations to achieve better environmental and financial performance. Thus, improving operations efficiency not only helps in reducing costs and increasing profitability, but also results in improved environmental performance.

We believe that most firms would be encouraged to improve environmental performance if there is a clear link or route by which these initiatives would improve their financial performance. And it is this link that this research has explored using operations efficiency as an intervening variable. This study found evidence of a significant moderating effect for operations efficiency on the environmental performance-financial performance link. This shows that the level of operations efficiency of a firm will affect the impact that environmental initiatives would have on its financial performance. We found that the impact of environmental performance on financial performance was strongest for firms with high levels of operations efficiency when compared with those with lower levels of operations efficiency.

What this means is that those firms seeking to improve their operations efficiency and their financial performance can invest in improving their environmental performance and vice versa. Simple housekeeping measures such as switching off lights and fans when not needed or more sophisticated design changes (e.g., design for disassembly - Shrivastava, 1995) for waste minimization can help firms not only reduce their costs of production but also improve their environmental/financial performance. Operations efficiency can also be improved using buildings and facilities with enhanced energy efficiency, redesigning production systems using cleaner technologies and more efficient production techniques, effective preventive maintenance strategies, systemic procedures for quality management, and, safer working conditions for employees (Shrivastava, 1995; Berman et al., 1999). Firms that proactively improve their operations, avoiding unnecessary waste (materials and energy), can also achieve better environmental performance as they will use less materials, produce less waste, use less energy and emit less pollutants. This is supported by the work of Doh et al. (2009) who found that improving operations efficiency co-varied with improving environmental performance and Triebswetter and Hitchens (2005) who found that high productivity plants implemented a higher number of environmental initiatives than low productivity firms. Therefore any firm seeking to improve its operations efficiency can also improve its environmental performance simultaneously, thereby leading to improved financial performance.

It should be noted that inasmuch as improvements in operations efficiency have a significant impact on environmental performance, it would not solve all environmental problems. This is echoed by Rothenberg et al. (2001) who suggested that these improvements (in the context of lean practices) would not be able to address all environmental issues.

Since investments in environmental performance just for the sake of it are more likely to have a negative impact on profitability, managers need to make investment decisions that provide improvements in both environmental performance and operations efficiency. This will help reduce the negative impact on profitability and lead to significant cost savings, which could then impact the bottom line positively.

3. Limitations and Scope for Future Studies

We have attempted to highlight the importance of operations efficiency and we have shown that operations efficiency moderates the relationship between environmental performance and financial performance. However, there might be other variables that also influence this relationship and this relationship could be even more complex. There could be curvilinear relationships between environmental and financial performance, which we have not addressed here. The presence of curvilinear effects could affect the returns from environmental/operational improvements and so further research would help highlight this. There could be mediating roles for other variables on this link. For example, the environmental technology portfolio consists of pollution-control technologies and pollution-prevention technologies (Klassen and Whybark, 1999; King and Lenox, 2002), and the link could be different if environmental performance is based on any one of them. Finally, our sample included only UK firms. It would be beneficial if this study is replicated in other national contexts to see if the relationships observed in this study are universal or country-specific. This moderating relationship can be analyzed across a number of years to identify changes over time. We welcome future research studies to take up these interesting issues.