The global Shariah Governance (SG) practices of Islamic Financial Institutions (IFIs) vary due to the legal rules in the country and the regulations to monitor the overall functions of Islamic banks and finance (Hassan et al., 2011). The governance structure is the written form of guidelines and practices by which the Board of Directors (BOD) ensures accountability, fairness, and transparency with the stakeholders (investors, customers, shareholders, management, employees, society and the government) related to the institution. The guidelines are delivered by the government and regulators to control the activities of the institutions and safeguard the interest of the numerous stakeholders. Accordingly, Ginena and Hamid (2015) illustrate SG as a complete system that outlines how IFIs follow the Shariah principles in conducting their business functions. Islamic Financial Service Board (IFSB) (2009) has defined SG systems as

However, Bangladesh has started its Islamic banking journey through the formation of the Islamic Bank Bangladesh Limited in 1983 (Hassan et al., 2017) with a combined effort of the government and its general people. Currently, Bangladesh has 8 Islamic banks, 19 Islamic banking branches and 35 Islamic banking windows to provide Islamic banking services (Bangladesh Bank, 2019). Though the central bank has promulgated a guideline in 2009, still Bangladesh has an absence of a well-defined full-fledged regulatory, supervisory specific, and structured governance framework to govern, supervise, monitor and regulate the Islamic banking activities (Ullah, 2014; Ahmad et al., 2014; Perves, 2015; Alam et al., 2019). Islamic banks have developed their own SG mechanisms due to the absence of a separate law and a complete SGF, which are flexible in their practice (Hassan et al., 2017).

Every Islamic bank has a different organizational structure and the SSB position is not the same and well organized (Alam et al., 2019; Perves, 2015). Therefore, numerous studies have recommended to legalize the existing Central Shariah Board for Islamic Banks of Bangladesh (CSBIB) or to set up a new Centralized Shariah Supervisory Board (CSSB) to monitor the overall functions, minimize the diversified Shariah resolutions and fatwas, reduce confusions about the banking practices and react against Shariah violations (Sarker, 2005; Ahmed & Khatun, 2013; Mamun, 2011; Ahmad et al., 2014; Ullah, 2014; Abdullah & Rahman, 2017; Hassan et al., 2017; Alam et al., 2019). These studies have not outlined the process to legalize the existing CSBIB or to form a new CSSB under the central bank. Therefore, the aim of this study is to explore the legalization status of a central Shariah regulatory authority for the Islamic banks in Bangladesh.

By carrying out the semi-structured interviews, we found diversified opinions about the research topic. The formation of CSSB and the legalization of CSBIB will be challenging without a separate Islamic banking act at preliminary stage but if the government and central bank are serious and committed to declaring the act; it could be done. The central bank and Islamic have limitations to form a CSSB, and even after forming CSSB, Islamic banks will be unable to follow the instructions of the CSSB. If the government modifies the existing law, it will rectify the problem to form CSSB under the central bank. The central bank can legalize CSBIB though a circular or can form a CSSB which will be considered as a lawful practice for the Islamic banks. Finally, the intention of the central bank and government is significant for such kind of initiative. In addition, Islamic banks need to prove their eagerness about the CSSB. To fulfill the demand and expectations of all concerned bodies, it is a prerequisite to institutionalize CSSB under the central bank for monitoring Islamic banks and their functions.

Our study has several contributions to the area of Islamic banking and SG literature in the context of Bangladesh. Besides, this research has implications for practitioners, regulators, and policymakers. First, this study illustrates the probable challenges to legalize the existing CSBIB or to form a new CSSB under the framework of the central bank. The formation of CSSB has been suggested by prior researchers (Ahmed & Khatun, 2013; Ahmad et al., 2014; Ullah, 2014; Abdullah & Rahman, 2017; Hassan et al., 2017; Alam et al., 2019). Second, the study explores that central banks or regulatory bodies can form a new CSSB if they really want to do so and thus can enhance SG functions. Third, this research broadens the existing literature on Islamic banking and its SG practices in relation to Bangladesh which will be helpful for the practitioners and policymakers to form a CSSB with legal power and responsibilities. Fourth, our study has significantly contributed to the agency, stakeholder and Institutional Theory (IT) by highlighting that the central bank has obligation to outline SG guidelines for the Islamic banks and numerous related parties to shelter the interest of stakeholders (Zahra & Pearce, 1989; BNM, 2010; Meyer & Rowan, 1977; Zucker, 1977; Scott, 2005). However, this research recommends Islamic banks and the concerned authorities should arrange Shariah related programs, and international collaboration with global regulatory authorities to improve on the limitations of SSB’s members and Shariah personnel.

The introduction will be followed by section 2, which will unfold the literature review of SGF of the Bangladesh and theoretical framework. Section 3 provides data collection methods and the analysis procedure for this study. Section 4 will outline the findings based on semi-structured interviews. Finally, section 5 will conclude with policy implications, recommendations, study limitations and future directions.

2. Literature Review & Hypotheses

2.1. Shariah Governance of Bangladesh

SG is an important component of Islamic banks which plays a significant role in policymaking and protecting the rights of shareholders and assures that all business activities, practices, and functions are in accordance with the compliance of Islamic principles (Hasan, 2011). In the governance system, BOD is responsible for the overall Shariah issues, managerial responsibilities and application of the suggestions of the SSB to protect and accomplish the demand of the concerned stakeholders (BNM, 2010; 2013, AAOIFI, 2010; IFSB, 2006). Management is liable for providing the reports of Shariah compliance to the BOD (BNM, 2010; 2013; IFSB, 2006). SSB members are employed by the BOD for monitoring the overall Shariah issues in the business functions, providing their Shariah views in Shariah related issues, and delivering an annual Shariah report on the overall functions (Zaidi, 2008). Besides, the complete roles of independent Shariah Supervisory Board (SSB) in Islamic banks are to assure that the functions of the Islamic banks are in compliance according to Shariah law and the need to publish the authorization report in the annual Shariah report (Briston & El-Ashker, 1986; Tomkins & Karim, 1987; Karim, 1990a, b; Rammal, 2006).

Bangladesh has a positive story in the growth and development of Islamic banking in relation to its market share and assets from its inauguration and positive growth. In the recent world financial crisis, Bangladesh is one of the few less affected countries probably due to the development of the Islamic banking system (Wasiuzzaman & Gunasegavan, 2013). In Bangladesh, almost all conventional banks are trying to operate Islamic banking branches and windows all over the country to attract the huge Muslim people (Rahman, 2014). In 2015, the central bank stopped issuing a new license to operate the Islamic banking branches and windows business parallel with conventional banking due to the Shariah issues. It has been opened later in 2018. Along with the progress, reposition and development, there is an absence of separate Islamic banking law to monitor the Islamic banks (Sarker, 1998; Ahmad et al., 2014; Alamgir, 2016; Hassan et al., 2017; Abdullah & Rahman, 2017).

As a banking regulator, the central bank outlines the rules and regulations for conventional and Islamic banks. Therefore, the central bank has issued the criteria for accomplishing the Islamic banking functions as per the Shariah law and the respective bank has to ensure all mechanisms conform to Shariah compliance (Bangladesh Bank, 2009). Unfortunately, the Bangladesh Bank has not created any Shariah department/division to monitor the Islamic banking activities and to guide SG compliance. Moreover, to complete Shariah compliance of Islamic banks, the central bank has not promulgated any guideline to assist the SSB though it is a significant issue for the banks (Hasan, 2014). Besides, the Central Shariah Board for Islamic Banks of Bangladesh (CSBIB) has started its operations in 2002 as a private organization for developing a unique SG practice in Bangladesh and performing its roles without an authorized body. Along with CSBIB, all Islamic banks have their separate SSB comprising with the prominent Shariah scholars with different names i.e. Shariah Board, Shariah Committee, and Shariah Supervisory Committee. Though all of the Islamic banks have SSB, only four banks have positioned SSBs in the organizational structure (Alam et al., 2019). Similarly, Islamic banking branches and windows also have SSBs with renowned Shariah professionals. SSB works as an oversight board for overall banking activities especially- day to day activities and performs Shariah audit and Shariah compliance review (Abdullah & Rahman, 2017).

Islamic banks in Bangladesh practice a mixed system of SG with respect to the rules and regulations, guidelines, SSB practices, and different ideologies. Moreover, Islamic banks are not bound to follow the overall standards and guidelines of the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) and International Financial Service Board (IFSB) (Bangladesh Bank, 2009; Hassan et al., 2017). Therefore, the absence of a separate Islamic banking law obstructs the effective functions and Shariah compliance activities of this industry (Ahmad & Hassan, 2007; Ahmad et al., 2014). In addition, SG is developed and practiced by the respective Islamic bank without proper monitoring and coordination from the central bank. The SSB of the individual bank is thus responsible for ensuring Shariah compliance within their own organizations and the central bank examines only the respective SSB reports of the banks (Sarker, 1998; Habib et al., 2013; Ahmad et al., 2014). The central bank does not have an independent CSSB to examine these reports or monitor the activities of SSB (Bangladesh Bank, 2009).

However, the formation of SSB is optional for the Islamic banks in the existing guideline of the central bank which contradicts the world practice (BMB Islamic, 2011). In this case, some claims that CSBIB fails to monitor and examine the current function of Islamic banks in Bangladesh because of some reasons such as its guidelines are not mandatory, the central bank does not recognize it and does not provide any support to use the guidelines. Due to such circumstances, CSBIB only provides an advisory service and monitors the activities of SSB as a private firm. Therefore, if any Shariah violations occur in the activities of the Islamic banks, CSBIB is not able to take any actions against the banks and CSBIB does not have the authority to solve the disputes among the BOD, SSB and the management in any Shariah related issues. All Islamic banks adhere to the resolutions of CSBIB in order to mitigate their reputational risk (Uddin, 2014) and this body does not have formal recognition from the central bank. Moreover, the BODs of Islamic banks are taking advantage of the central bank SG guideline (Hassan et al., 2017). They also state that SSB members do not have the responsibility regarding the Shariah compliance and presume that they desire to move the responsibility to the BOD. Therefore, it is important to place CSSB under the structure of the central bank for monitoring Shariah issues of Islamic banks, SSBs, resolving disputes among SSBs, providing unique Shariah resolutions and taking actions against Shariah violations.

SG is regarded as an important mechanism for Islamic banks to accomplish accountability (Grais & Pellegrini, 2006a). Prior studies in this area (see for example. Grais & Pellegrini, 2006a; Abu-Tapanjeh, 2009; Bhatti & Bhatti, 2009; Kasim et al., 2013) recommend that information and transparency regarding Shariah compliance is progressively demanded by numerous stakeholders and by society at large. In examining the SG concerning the managerial frameworks, prior researchers (e.g., Hasan, 2011; Obid & Naysary, 2014; Al-Nasser Mohammed & Muhammed, 2017) have used mainly three theories namely agency theory (Jensen & Meckling, 1976), stewardship theory (Donaldson & Davis, 1991); and stakeholder theory (Freeman, 1984). It is well acknowledged that agency theory places emphasis on the predetermined or governing relationship between the principal and agent. The theory focuses on the concepts and solutions such as (1), the conflict of interest concerning the agent and the principle, (2) information asymmetry, and (3) concerns of risk tendency (Jensen & Meckling, 1976).

Agency theory, as applied in CG, suggests that

As Islamic Banks, SSBs and managers are not merely accountable to the corporation or stockholders but also to God, along with the consideration for social objectives (Kamla et al., 2006; Abu-Tapanjeh, 2009), it is contrary in relation to the self-opportunistic view prescribed under an agency theory. It does not explain that the owner’s interest in ignoring Shariah as Islamic regulations in the application of the assets and contractual privileges (Bhatti & Bhatti, 2009). Consequently, the authentic report along with all Shariah principles help to enhance the faith and confidentiality of the general public, depositors, agents and stockholders to minimize information asymmetry amongst the management and other related parties with regards to the institutions operational functions (Grais & Pellegrini, 2006a; Archer & Karim, 2007; Vinnicome, 2010). Moreover, the owners and depositors should have the accessibility of authentic and trustworthy information; thus for religious matters, transparency is not only required but essential in Islamic Banks (Haniffa & Hudaib, 2007).

In addition, Institutional Theory (IT) deliberates on the process by structures containing application which are regulative, normative and cultural cognitive. It is recognized as commanding strategies for societal behavior. IT has become popular because of the general and dominant description of guidelines for both individuals and corporations (Scott, 2005). In addition, Meyer and Rowan (1977) and Zucker (1977) have drawn a novel tactic of an institutional predictor that emphasizes the social character and perception in an institutional enquiry. Meyer and Rowan (1977) highlight that organizational guidelines work as mythologies through incorporated institutions, legitimacy, acquisition, constancy, and improved survival prospects. In this case, SGF also provides the overall guidelines, strategies, and procedures for Islamic banks to conduct, monitor and control their activities. This suggests that rational ideas of corporations are the key power for institutions to adjust applications and processes to improve their legitimacy and existence (Meyer & Rowan, 1977). Therefore, the CSSB provides Shariah resolutions based on the Islamic principles concerning the conflict and referred issues from the Islamic banks.

Governance structure ensures justice among the stakeholders is practiced over the improvement of transparency and responsibility (Majeed, Aziz, & Saleem, 2015) by stimulating Islamic principles i.e. justice, Shariah compliance, zakah management (Mittal, Sinha, & Singh, 2008). Moreover, the SG structure describes the boards association, formation of various committees along with SSB members, management and exchange of information amongst them (Zahra & Pearce, 1989). IT endeavors to outline more essential features of how institutions are shaped, continued, altered and postponed, and contracts with the pressures of IFIs on human behavior in their practices i.e. guidelines, practices and the norm of social behavior. Numerous organizational logics are submitted for institutions and persons, and the related parties in organizational logics acknowledge without prejudice the independence for institutions and individuals.

Due to the absence of an instrument to control the organization or governance procedure (as SSB or CSSB), the confidence of the general public towards the Islamic banks legitimacy and validity of the products may decrease (Chapra & Ahmed, 2002). In this regard, the SSB is considered crucial in SGF of Islamic banks. The role of SSB is to monitor the overall Islamic banking activities independently in relation to Shariah rules and regulations. Consequently, from the stakeholder perspective, SG plays a role similar to CG that is also used to estimate the compliance of the overall activities in order to confirm Shariah principles are upheld. SG is directed by a complete set of SGF which provides a comprehensive structure of roles and responsibilities for all related parties (management establishment, and affairs of the SSB). This includes Shariah compliance guidelines of Islamic banking practices in relation to the Shariah rules.

However, in protecting the rights of stakeholders and as the controlling mechanism of SG, managers have to perform a vital role in implementing Shariah rules and monitoring the banking activities. In IFIs, managers must be accountable to Allah, not only to shareholders and the company with the final objective of well-being and accomplishment for humanity (Abu-Tapanjeh, 2009) which is a default idea from the self-interest concept prescribed by the agency theory. Consequently, the aim of the particular observing process of SG is to confirm compliance among Islamic banks in relation to the ideologies of Shariah and to prepare Shariah complaints report which may play a significant role towards owners, and other stakeholders (Grais & Pellegrini, 2006a). An organization is not only involved in the structures, procedures and processes of a particular institution but also for numerous institutional structures that are practiced together to attain a mutual goal such as to stimulate sound SG practices or to articulate the standards of accounting and applying them in their practice.

However, IT refers to the ability of the countries and institutions to implement similar (SG) structures and exercise as isomorphism (DiMaggio & Powell, 1983). Carpenter and Feroz (2001) describe this procedure as organizational marking and they claim that this procedure does not essentially make institutions more effective. Further, Carruthers (1995) claims that the institutional procedure is a social and political issue that denotes legitimacy and authority much more than effectiveness alone. Thus, the countries and institutions can implement particular SG exercises not only for the enhancement of performance or to drive financial development but also to attain legitimacy in the particular society. In this regard, the absence of CSSB and self-developed practices create confusions amongst the customers, general people, businessmen and governments about the Islamic banking functions in Bangladesh (Ahmad et al, 2014; Abdullah & Rahman, 2017; Sarker, 1998). Therefore, the failure to confirm Shariah principles could expose the IFIs to reputational risk both to the individual institution and the overall industry (Grais & Pellegrini, 2006b).

To accomplish the research objective, the researchers have investigated the answer to “what are the way to legalize the CSBIB or to set up a new Centralized Shariah Supervisory Board for Islamic Banks in Bangladesh under the central bank?” Therefore, a qualitative research is applied as it helps to understand how and why things occur (Cooper & Schindler, 2011). It comprises

The semi-structured interview is selected by the researchers to extend more data connected to the study and thus gain a wider understanding –of– the practical aspect of the subject matter. Semi-structured interview denotes to the interview whereby

A face-to-face interview technique has been applied to collect the data since it is more comfortable to achieve a clear understanding of the research topics. When an interview is conducted face-to-face, it assists to stimulate the depth replies from the participants. This procedure helps the respondents to understand the questions more clearly (Sekaran & Bougie, 2003). A face-to-face interview protects the individuality of the respondents in outlining their views which are vastly valued for the quality and authenticity in the data collection process (Kvale, 1996; Gillham, 2000; Sekaran & Bougie, 2003). Therefore, the respondents are directly related to policymaking, and the function of SGF in the Islamic banks. Moreover, they have vast knowledge, familiarity, and practical experience in relation to Islamic banking activities and its SG. 17 respondents are interviewed who are directly related to the central bank, Islamic banks, SSB, Shariah department and SG. The respondents are given symbolic identity to keep their confidentiality namely ‘RA’ (Regulatory Aspects) from the central bank, ‘SP’ (Shariah Practitioners) from the Islamic banks and lastly ‘E’ (Experts) who are related with the industry and research in this field.

The NVivo has been applied for analyzing the huge textual data in qualitative research, as it permits more in-depth analysis and delivers more advanced tools to envisage data (Patton, 2002; Gibbs, 2002). NVivo software is used as a comprehensive technique to decode, categorize and create themes (Strauss, 1987; Joffe & Yardley, 2004). It allows green data management and analysis tools rather than paper and pencil techniques. Initially, the researchers identify the fruitful outcomes from the gathered data. The findings of the analysis are discussed below.

4. Discussions of the Findings

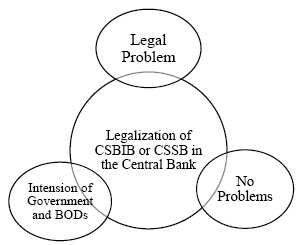

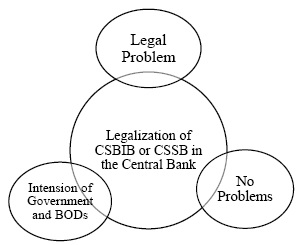

Based on the perceived data and data analysis regarding the legalization process of CSBIB or the formation of CSSB in the central bank, this study has identified three categories which are shown in figure 1 which consists of legal problem, no problems, and lastly, the intention of the government and Islamic banks. The discussion part also identifies the probable challenges of the legalization of CSBIB or CSSB which are described below.

This research articulated diversified opinions regarding the legalization of CSBIB or the formation of CSBB. One of the respondents from the regulatory side opines that without the law, it will be difficult to institutionalize CSSB under the central bank. Moreover, the current culture of Islamic banking practices and the central bank environment are not ready for the legalization of CSSB.

In addition, the legalization of the existing CSBIB is difficult because of its nature and it is not similar to CSSB structure like Malaysia, and Bahrain. Thus, the government intention is important in establishing CSSB under the central bank. The establishment of CSSB with legal power in the central bank will fulfill the demand and expectations of all Islamic banks, the general public, and concerned stakeholders. Therefore, if the government wants to set up CSSB in the central bank, another challenge is the lack of experienced SSB members for CSSB.

Conversely, respondents (E#1; RA#2, 3) opine there is no problem and conflict in setting up a new CSSB or legalization of existing CSBIB under the central bank with proper power and authority within the boundary of CSGF.

Besides, the government can modify the existing body or can keep it as an advisory body or form a new CSSB under the monitoring of the central bank which would not be a problem. In this regard, the government needs to amend the banking company act to set up a new CSSB under the central bank. Moreover, the existing banking company act authorizes the central bank to provide any circular regarding banking issues and it will be considered as an act. Thus, it is not a problem to form CSSB.

The regulator can legalize the existing CSBIB or set up a new CSSB through a circular which will help the central bank to monitor the overall Shariah issues. Besides, to form CSSB will be time consuming as it is related with the government law, legal issues and sentiment.

The discussion has explored the possible way to legalize the existing CSBIB through a circular or form CSSB under the central bank for the overall monitoring of the Islamic banking functions provided the government or the central bank agrees to do it.

5. Conclusions and Recommendations

The central objective of the study is to find out the formation process to legalize the existing CSBIB or to set up a new CSBB for Islamic Banks in Bangladesh. Based on the results of the semi-structured interviews, the study found diverse opinions regarding the legalization of CSBIB or the formation of CSSB to control the central bank. Primarily, it will be difficult to set up CSSB under the central bank and the existing Islamic banking system is not ready for it. In addition, the legalization of CSBIB is quite difficult because the structure of CSSB in Bangladesh is different from Malaysia, or Bahrain. In order to empower CSSB, the government aspiration and political will are important factors.

In Malaysia, the government establishes CSSB at its central bank directly supporting this industry (Abdullah and Rahman, 2017). Conversely, a few of the respondents opined that there are no problems in the legalization of the CSBIB or the formation of CSSB under the central bank with legal power and authority in the guideline of CSGF. The government can modify the existing CSBIB or transform it as an advisory body by establishing a new CSSB under the central bank. The government can also modify the existing banking law or the central bank can also consider the legalization of CSBIB as obligatory for Islamic banks. Therefore, if the government or the regulatory authorities are really interested, they can prepare a circular to legalize the existing CSBIB or formulate CSSB under the central bank. Another problem is the absence of a Shariah knowledgeable candidate or an expert in the field to form the CSSB in Bangladesh. For the time being, the regulators will be able to solve this problem through initiatives such as training programs, seminars, conferences, and professional courses. Finally, the formation of CSSB under the management of the central bank will fulfill the demand and expectations of Islamic banks and their numerous stakeholders. The concerned regulatory authorities should prioritize Islamic banks SG guidelines and regulations as it holds the one-fourth of the overall banking industry.

Our research has several contributions and implications for the regulators and Islamic banks in Bangladesh. First, this is the first study that has outlined the probable way to legalize the CSBIB or form CSSB in the management of the central bank of Bangladesh. Second, the study broadens the literature on Islamic banking and SG in relation to Bangladesh which will be helpful to the regulators and government to fill up the information in the formation of CSSB. Third, the findings of this study can be a potential source of knowledge for regulators and the central bank of Islamic banks in legalizing the existing CSBIB or to form a new CSSB under the management of the central bank for monitoring the Islamic banks and homogeneous SG practices. Fourth, our study has contributed to the agency, stakeholder and IT by illustrating the roles, power, functions, and accountability of the concerned stakeholder and Islamic banks.

The central bank is responsible to provide guidelines for all concerned bodies to protect the interest of all stakeholders (Zahra & Pearce, 1989; BNM, 2010; Meyer & Rowan, 1977; Zucker, 1977; Scott, 2005). Where-, SSBs should perform their roles with proper independence and the stakeholders have the right to know the actual practices of SG and Shariah compliance (Haniffa & Hudaib, 2007). The absence of CSSB and particular guideline create confusion and minimize the confidence of stakeholders (Alam et al., 2019; Hassan et al., 2017; Ahmad et al., 2014; Abdullah & Rahman, 2017; Sarker, 1998). Finally, the central bank can legalize the CSBIB or for a new CSSB through a circular which will also be considered as a mandatory guideline for the Islamic banks.

The research applied a qualitative study rather than a quantitative method to explore the possible way to legalize the CSBIB or to set up CSSB under the supervision and instructions of the central bank of Bangladesh. Initially, the study is limited to Islamic banks in Bangladesh. Secondly, the researcher is unable to access the central bank as the Human Resource Department does not allow data collection. As Bangladesh does not have CSSB for Islamic insurance, and Islamic cooperative societies, it is recommended to investigate the formation procedure of a central authority for the particular industry. Future researchers could also investigate the possible challenges for such kind of formation in other jurisdictions such as Saudi Arabia, Sri Lanka, India, and the United Kingdom as the present study does not include these countries in the research scope. Future research can also apply the same methodology or use the quantitative tactic for data collection.